Solar Tax Benefits Guide

Key highlights:

Renewable energy is experiencing a surge in popularity — just look around and count how many homes on your street now have rooftop solar panels. This growth isn’t just limited to consumers; builders and purchasers are increasingly getting involved. This is unsurprising; since 2022, the U.S. government has significantly ramped up incentives for green energy through the Inflation Reduction Act, making solar projects more appealing than ever. The current administration has passed a new tax bill on July 4th, 2025 and decided to keep these Investment Tax Credits incentives till 2027.

As a result of these shifts by IRA, solar energy projects have become increasingly attractive for solar purchaser, both socially and financially.

The potential financial returns are significant: For a typical high earner, purchasing a solar energy project can increase take-home income by 50% or more. And these benefits apply broadly; they can reduce all forms of personal and business taxable income, including income from salary, RSUs, a bonus, business profits, capital gains, and other sources.

In this guide, we’ll explore the financial benefits of solar projects, the process of buying in, the risks, a real-life example, and a few other considerations.

The Benefits of Buying a Solar Project

Purchasing solar projects offers three major benefits.

Investment Tax Credits

A tax credit is a dollar-for-dollar reduction in the amount of taxes you owe. It is similar to a gift card or store credit you can use to reduce your tax bill.

For example: if you owe $1,000 in taxes and you have a $600 tax credit, your tax liability will be reduced to $400.

The government typically offers tax credits to incentivize certain behaviors or purchases. Over the last few years, tax credits have become an increasingly popular tax-mitigation tool due to incentives tied to renewable energy.

Depreciation

Depreciation is the amount of value that a physical asset loses over time. From a tax standpoint, it’s important because you may be able to take a deduction for this amount, reducing your taxable income and saving money on your taxes.

Example: Suppose you earn $2 million in income and, at the highest federal marginal tax rate of 37% (ignoring state taxes for this example), would owe about $740,000 in federal taxes. If you had $500,000 in depreciation, you could use it to reduce your taxable income by that amount—bringing it down to $1.5 million. At a 37% tax rate, that would save you roughly $185,000 ($500,000 × 37%) in federal taxes.

Income Stream

Solar projects typically include 20-30 year income streams tied to the energy produced by the project. These returns depend on the location of the project and local energy rates among other factors but typically will generate between 1-5% annually of your purchase amount.

Popular Solar Structures

Now that you understand the general benefits of buying solar projects, let’s talk about the different structures available.

The three most popular structures are flip partnerships, sale-leasebacks, and asset purchases. Below, we will explain how each structure works and their financial benefits, risks, and comparisons. You can also read our in-depth article about them here.

Flip Partnership

A flip partnership is a partnership between a solar purchaser and a solar developer — where both form a legal partnership to jointly own a solar project. The name comes from the way ownership “flips” over time between the two partners.

Here’s how it works:

This structure uses leverage to enhance tax benefits. The purchaser puts in a $1, and the developer contributes another $1 in debt, bringing the total partnership value to $2.

For the first 5–6 years, the solar purchaser typically holds 99% ownership in the partnership. This structure allows the solar purchaser to claim 99% of the tax benefits, which are fully vested over this initial 5–6 year period.

After the 5–6 years, the partnership flips: the solar developer becomes the majority owner (usually around 80–95%), and the solar purchaser’s becomes the minority owner (typically 20–5%. By this stage, all tax incentives have been fully vested and claim by the purchaser, so the project primarily generates cash flow moving forward. That cash flow is distributed based on the updated ownership percentages, with the majority going to the developer.

This is considered a fair trade-off: the purchaser receives nearly all the tax benefits up front, while the developer receives the majority of the cash flow after the flip.

Who is this for?

Flip partnerships are a particularly good fit for individuals and businesses aiming to offset more than $500,000 in annual income.

What are the financial benefits?

You can read about a real-life flip partnership case study here.

Solar Sale-Leaseback

A sale-leaseback is a structure in which a solar developer sells a solar project to a solar purchaser and then leases it back from them. This way, the solar purchaser benefits from tax incentives and a steady income stream from the project with minimal overhead, and the solar developer operates the system, maintains the system and make a profit based on the spread between the price at which they sell the electricity and the price at which they pay the solar purchaser.

Who is this for?

Solar sale-leasebacks are a good fit for individuals who want steady cash flow and/or have smaller tax write-off needs.

What are the structure’s financial benefits?

Solar Asset Purchases

A solar asset purchase is a structure where the solar purchaser buys the solar system outright and becomes its sole owner. Unlike other structures, there’s no partnership with the developer—the purchaser is fully responsible for the project, including all liabilities. While operations and maintenance (O&M) are typically handled by a third party, the owner can choose to manage the project themselves or hire an O&M company.

This structure allows the purchaser to benefit from both the tax incentives and the long-term cash flow, but also requires them to take on all administrative and operational responsibilities.

Who is this for?

Solar asset purchases are a good fit for individuals or businesses who want full ownership and control over the project and are comfortable handling (or outsourcing) its day-to-day operations.

What are the structure’s financial benefits?

- Tax incentives: The purchaser can claim the full tax benefits, which can significantly reduce their tax bill.

- Stable income: Since there’s no developer or partner involved, the purchaser keeps 100% of the income generated from the project.

Navigating the Risks and Limits of Solar Projects:

While the benefits of solar projects are significant, it’s equally important to understand the potential risks and constraints involved.

Material Participation Requirements

The IRS categorizes income into two buckets: active income (e.g., W-2 earnings, income from a business you actively run) and passive income (e.g., rental income from property you don’t actively manage). Importantly, tax benefits must match the character of income — passive losses can offset passive income, and active losses can offset active income, but the two can’t cross.

Solar follows the same rule. If you want to use the tax benefits from solar to offset active income, you must be active in the solar space. So, you will need to set up an LLC through which you will make your purchase, and you will also need to materially participate in the solar business. In this context, “material participation” means participating in the solar space for more than 100 hours during the tax year in activities that are considered regular, continuous, and substantial, and participating at least as much as any other individual involved in the business.

(Note that this is not true for investments in oil and gas wells due to a unique law benefiting the space, so that can be a viable alternative if you are unable to qualify as an active participant in solar. Note also that those with passive income can use the benefits of solar without qualifying as an active or material participant in the solar space.)

Why is this a gray area? The IRS and tax court have not defined what specific activities constitute material participation in the solar space. However, the national accounting firm that we work with recommends thinking about it from a business owner standpoint, not from an investment standpoint — you are building a fact pattern of activities as someone who owns and operates a solar business, not someone passively holding an asset. Your CPA or tax advisor, along with the developer’s accounting team, can help you determine what satisfies the 100-hour requirement based on your individual situation.

(This is a very simplified explanation. For more details on material participation and common questions we hear from CPAs, check out this article.)

A quick note on tracking: Valur provides a platform where you can save relevant documents and log your participation hours directly. This makes it easier to maintain organized records for tax filing purposes. Read more about those tools here.

Developer / solar project risk

When purchasing a solar project, the experience and reliability of the developer are critical. To qualify for tax credits and depreciation in a given tax year, the project must reach “Mechanical Completion” within that same year. In practice, this means you’ll be buying new projects—not ones already in operation—and they must be both mechanically complete and placed in service in the same calendar year in which you plan to claim the incentives.

Once placed in service, the project must remain operational for at least five years and one day to avoid tax credit recapture.

Because of this, it’s essential to prioritize:

- Projects with a realistic, well-defined construction timeline that ensures completion in your target tax year.

- Developers with a proven track record of delivering on time and as promised.

- Clear plans and safeguards—both from you and the developer—to ensure the project operates for at least five years and one day without disruptions that could jeopardize compliance.

Depreciation and tax credit cap

Depreciation for solar purchasers who want to apply it against W‑2 income (i.e., salaried income) is capped at $256,000 per individual or $512,000 per couple per tax year (adjusted annually for inflation) due to the excess business loss limitation. Any unused depreciation in a given calendar year can be carried forward to future tax years.

Importantly, if you are a business owner — with either active or passive business income — there is no limit on the amount of depreciation you can apply.

Tax credits work differently. The amount you can use in a given year is limited to 75% of your remaining federal tax liability after applying depreciation. Any unused credits can be carried forward and applied against your taxes for the next 15–18 years.

Real-Life Example

Lara is a tech executive living in California, married filing jointly. In 2026, she will earn $2,000,000. As a result, she expects to have a substantial tax bill of approximately $1,006,000 in federal and California taxes in 2026 (assuming she falls into the highest federal marginal tax bracket of 37% and California’s highest marginal tax rate of 13.3%). After paying total taxes, that would leave Lara with $994,000.

However, buying a solar flip partnership project could earn Lara significant tax credits, depreciation deductions, and ongoing income to mitigate her high tax burden.

Specifically, imagine that she chooses to contribute $300,000 in a flip partnership solar project this year. As a result, Lara could reduce her tax bill in 2026 from $1,006,000 to up to $576,776 and also reduce it by up to $63,202 more in the following 5 years.

Let’s now see the numbers:

Situation Overview:

- Income: $2,000,000 in 2026

- Expected taxes without solar benefits: $1,006,000

Solar Impact:

- Purchase amount: $300,000

- Tax Savings: up to $429,224 in year 1

Results:

Total tax savings: As a result of her solar purchase, Lara’s total tax bill will come down from $1,006,000 to $576,776 in year 1. That’s a total reduction in federal and state taxes of up to $429,224 in year 1, or 143.1% of the $300,000 purchase amount.

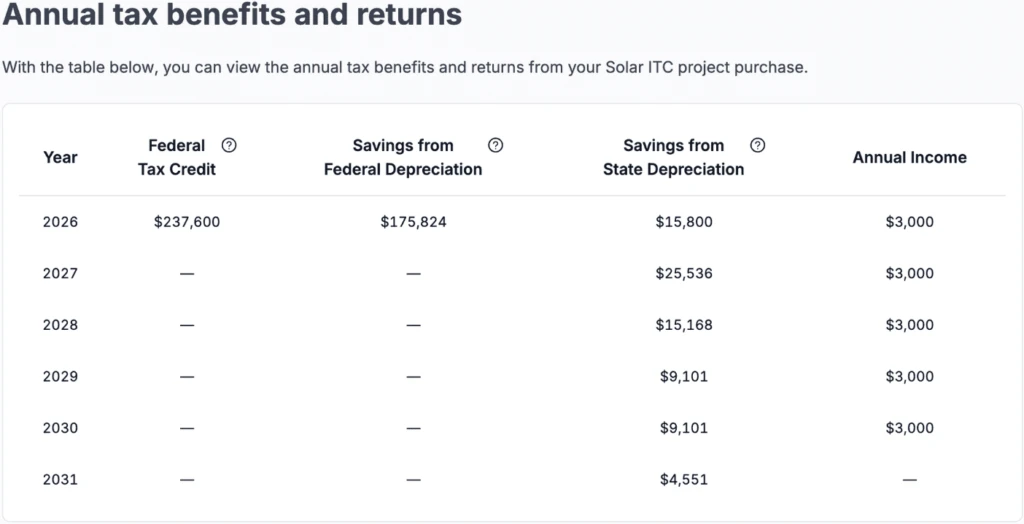

- Tax Credits: $237,600 in tax savings in the first year, or 79.2% of the purchase amount.

- Federal Level Depreciation: $175,824 in tax savings, or 58.6% of the purchase amount. (100% of this depreciation credit is available in year 1; federal depreciation saving calculations are based on highest federal marginal tax rate of 37%.)

- State Level Depreciation: $79,002 in tax savings, or 26.3% of the purchase amount. (Up to 20% of this depreciation credit is available in year 1, and the remainder will be spread over the following five years; state depreciation saving calculations are based on highest state marginal tax rate of 13.3%.)

Year-by-Year Tax Savings:

Below, you can see the year-by-year tax savings from tax credits and Federal and State depreciation for Lara taking into account their particular situation.

See your potential savings with your own numbers using our online calculator here.

Tax credits and depreciation are subject to limitations based on the type and amount of income you’re applying them against in a given calendar year. However, any unused credits or depreciation can be carried forward to future years—they don’t expire or get lost. You can read more about these limitations [here].

Total Income: In addition to tax benefits, this strategy includes a cash flow component. Estimated distributions are around 1% of the purchase amount, which would be roughly $3,000 yearly and about $15,000 total over six years on a $300,000 purchase amount. While projections are subject to variation, these estimates are based on typical performance and current tax law.

What if Lara chose not to purchase a solar project?

This is, of course, a common question: How would she do if she simply paid her taxes and invested the remaining money? This is a pretty simple comparison as if Lara doesn’t put $300,000 into the solar project, she would owe more than that in taxes. Given that her income is $2,000,000.

Situation Overview:

- Tax bill: $1,006,000

- Amount not put in solar: $300,000

- Total Missed Tax Savings & Cashflow from Solar: up to $507,426

- Net Loss: -$207,426

Results:

If Lara simply paid her taxes, she’d owe the full $1,006,000. By contrast, participating in the flip partnership would generate about $507,426 in tax savings and cash flow. Subtracting the $300,000 cost of the solar purchase, that’s a net gain of $207,426 compared to doing nothing.

The key point: the $300,000 she put in solar is money she’d otherwise send to the IRS and never get back. Instead, solar allows her to redirect those “lost dollars” into something that generates additional tax savings, produces cash flow, and contributes to a cleaner environment.

Some people try to compare this to investing the same amount in the stock market—but that’s not an apples-to-apples comparison. You invest after-tax dollars in the stock market. With solar, you’re putting pre-tax dollars—money you’d otherwise send to the IRS—to work for you.

Not bad results at all! And you can also play with our online calculator to customize it with your own numbers and see your potential savings here.

If you’d like to read a more detailed example, please read about Priya’s case here. We also invite you to read another example of how Aaron managed to significantly his taxes by purchasing solar projects.

Conclusion

Purchasing solar projects can be an effective strategy for high-income earners with significant ordinary income to reduce their tax liability.

How can you go about buying qualified projects? It’s relatively simple: Valur has partnered with reputable developers to make solar projects accessible to high-income earners. We help you identify and evaluate available opportunities, compare different project options, and visualize the potential benefits—using a calculator tailored to your specific income situation.

From there, we’ll help you seamlessly finalize your purchase—with no fees charged to you by Valur.

To learn more you can schedule a call with us here.

Need some help to understand which if this is the right fit for you?

Explore the solar projects available for you on our platform!

About Valur

We’ve built a platform that makes advanced tax planning – once reserved for ultra-high-net-worth individuals – accessible to everyone. With Valur, you can reduce your taxes by six figures or more, at less than half the cost of traditional providers.

From selecting the right strategy to handling setup, administration, and ongoing optimization, we take care of the hard work so you don’t have to. The results speak for themselves: our customers have generated over $3 billion in additional wealth through our platform.

Want to see what Valur can do for you or your clients? Explore our Learning Center, use our online calculators to estimate your potential savings or schedule a time to chat with us today!

Reduce your tax bill — fast

Our team of experts will help you evaluate the most promising strategies in minutes.

Talk to our expert team

Valur

Most Promising Fintech Companies 2024

On this page

Ready to talk through your options?

Free 15-min consult · No obligation · Featured Article