Exchange Funds: How They Work, Tax Benefits, and Whether They’re Right for You

Exchange funds let investors diversify a concentrated stock position without immediately triggering capital gains taxes. Instead of selling appreciated shares and writing a large check to the IRS, you contribute your stock to a fund and receive a diversified basket of holdings in return. The tax bill is deferred, not eliminated; but that delay can be worth hundreds of thousands of dollars in additional compounding growth.

An exchange fund (also known as a swap fund) works similarly to a mutual fund; it pools assets from multiple investors into a diversified portfolio, but instead of contributing cash, you contribute stock. That single distinction is what makes the tax deferral possible.

Key Takeaways

Designed for investors who find themselves holding a single stock worth $1 million or more with a very low cost basis. This includes tech executives and employees sitting on vested equity or restricted stock units (RSUs), founders who retained shares following a partial liquidity event, and retail investors holding a position that has appreciated significantly over the years.

Exchange funds are only appropriate for those who have no need to access the capital for at least seven years, and for whom high fees are not a concern.

An exchange fund can accomplish two important things at once: diversification of a concentrated position and deferral of taxes, without requiring a sale.

Because your full pre-tax amount stays invested and compounding from day one, the financial advantage compounds significantly over time. For example, a $5 million position can generate more than $2 million in additional wealth over 20 years compared to selling and reinvesting after taxes.

What Are Exchange Funds?

An exchange fund, or swap fund, is similar to a mutual fund but, instead of contributing cash, investors contribute stock. By aggregating the concentrated stock positions of many investors, an exchange fund allows you to substitute or replace your own concentrated stock position with a diversified basket of stocks of the same value, reducing portfolio risk and putting off tax consequences until later. Importantly after you have exchanged your concentrated position for a diversified basket of stocks you will still have to pay capital gains taxes when you sell the diversified stocks (unless you use a Charitable Remainder Trust) but because you now have a diversified basket of stocks it is less pressing for you to sell your shares and face the capital gains taxes.

Not sure which strategy applies to your situation? Valur’s guided planner can help you identify the right approach in minutes and at no cost.

This guide covers everything you need to know about exchange funds: how they work, their real costs and limitations, a concrete example of the math, and how they compare to alternatives like Charitable Remainder Trusts.

How Do Exchange Funds Work?

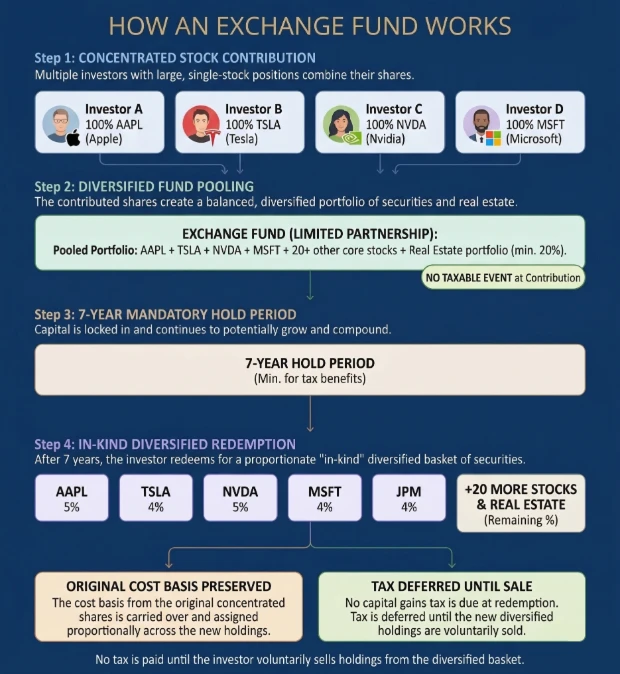

When you contribute your shares to an exchange fund, no sale takes place. Instead of a traditional sale of assets, the transaction is structured as an investment in a limited partnership rather than a taxable exchange. That distinction is everything.

The Basic Mechanics

You and a group of other investors each bring your concentrated single-stock positions to the pool. The fund aggregates those positions into a diversified portfolio — typically 20 or more securities, plus a real estate component that satisfies IRS requirements for tax-deferred treatment — and you receive a share of that portfolio proportional to your contribution. Your full investment amount stays working from day one, and as the assets in the portfolio grow, so does your stake.

After a mandatory seven-year hold period, you may request a distribution of a proportionate basket of the fund’s diversified holdings. Those shares will retain your original cost basis, and your capital gains remain tax deferred until you choose to sell.

The 20% Illiquid Asset Requirement

To qualify for tax-deferred treatment under IRS rules, exchange funds must hold at least 20% of their portfolio in illiquid assets. This requirement exists to prevent the structure from being used purely as a tax-avoidance vehicle. Most fund managers satisfy this by including real estate investment trusts (REITs) or direct property holdings alongside the contributed stock positions.

What Happens to Your Cost Basis?

Your original cost basis does not reset when you contribute to an exchange fund or when you receive your diversified basket of stocks at redemption. The low basis you carried on your original concentrated position is preserved and assigned proportionally across the basket of stocks you receive. Basis tracking is the responsibility of your CPA, not the fund manager, which can add some administrative complexity.

Is an Exchange Fund the Same as an ETF?

No. An exchange-traded fund (ETF) is a publicly traded security you buy and sell on a stock exchange. An exchange fund is a private limited partnership to which you contribute stock. The word “exchange” refers to swapping your concentrated position for a diversified one, not to a stock exchange. They are completely different structures.

The Tax Benefits of Exchange Funds

The primary tax advantage of an exchange fund is deferral. Rather than selling appreciated stock and paying federal long-term capital gains tax (currently up to 23.8% including the Net Investment Income Tax) plus applicable state taxes, you defer that liability indefinitely — or even permanently, if your heirs inherit the holdings and receive a stepped-up basis.

For a $5M position with a very low cost basis in a high-tax state, the immediate tax bill on a sale could easily exceed $1.5M. Keeping that capital invested and compounding for 7–20+ years can generate significantly more wealth than paying the tax and reinvesting the proceeds.

Exchange Funds for Concentrated Stock Positions

The risk of holding a concentrated position is well-documented: a single company’s stock can lose a significant chunk – or even all – 50%, 80%, or 100% of its value regardless of how strong its long-term story appears. Diversification is the rational move, but the tax cost of selling makes it painful to act. Exchange funds solve this by allowing you to diversify the economic risk without triggering the tax event.

Exchange funds are designed for investors with large, low-basis concentrations in a single stock. This is a common situation for company founders, long-tenured executives, tech employees with equity compensation, and anyone who has held a single position for years. They work equally well for inherited positions where family wealth remains concentrated in a single holding.

Although these are all potentially qualified candidates, the feasibility of this strategy will depend on which stock they hold; most exchange funds accept only shares from mid- and large-cap public companies, and many will only absorb a portion of your position rather than the full amount.

Exchange Funds: A Real-World Example

Say you hold $5M in a single public company stock with a near-zero cost basis. If you sell to diversify, you’re looking at approximately $1.5M in combined federal and state taxes depending on your state of residence. That’s capital that will never compound for you or your heirs.

Using an exchange fund, you contribute the $5M position, avoid the immediate tax event, and enter a diversified portfolio. The fund charges annual management fees of roughly 1.50%–2.00%, or $75,000–$100,000, per year (though this is declining; some public stock exchange funds now charge closer to 0.80%).

After 20 years, assuming a standard growth rate, you can see the over $2M+ growth this process earned:

| Sell & Reinvest | Exchange Fund | |

|---|---|---|

| Starting capital invested | ~$3.5M (after $1.5M tax) | $5M (full amount) |

| Annual fees | ~0.10–0.20% (index fund) | 0.80–1.50% |

| Value after 20 years (pre-tax) | ~$16.3M | ~$18.5M |

| Advantage | — | +$2.2M (+13%) |

| Assumes 7% average annual growth rate. Figures are illustrative. Actual results will vary based on portfolio performance, fee structure, and state tax rates. | ||

Want to see what this looks like for your specific position? Use Valur’s capital gains tax planning calculator to estimate your potential savings in under a minute.

Exchange Funds: Pros and Cons

Pros

- Immediate diversification without triggering a taxable sale

- Full investment amount stays working with no upfront tax drag

- Indefinite capital gains deferral, with potential stepped-up basis for heirs

Cons

- Seven-year lock-up with no access to capital. Early exit typically means receiving the lesser of your original stock value or current fund value, while forfeiting tax benefits and still paying applicable fund fees.

- Ongoing management fees of 1.50–2.00% annually for traditional funds, with newer platforms ranging from 0.80–1.25%. Costs compound over time and can erode the tax deferral advantage on very long hold periods.

- Limited access and partial acceptance. Funds are structured as private limited partnerships that close once they hit capacity, most accept only mid- and large-cap shares, and they may absorb only a portion of your position.

- Contribution minimums of $1M or more for most funds, with some platforms accessible starting at $100,000.

At Valur, our platform handles the complexity, from strategy setup and legal documentation to ongoing administration, so you’re not navigating this alone.

Is an Exchange Fund Right for You?

The ideal candidate checks most or all of these boxes:

- Holds a single stock worth $1M or more with a very low cost basis. This is typically shares accumulated over many years, not recently purchased.

- Doesn’t need access to the capital for at least seven years. This disqualifies anyone who might need liquidity for a home purchase, business venture, or retirement income in the near term.

- Wants the assets to pass to heirs

- Is an accredited investor. Exchange funds are private partnerships accessible only to qualified investors.

- Holds shares in mid- to large-cap public companies. Most funds won’t accept small-cap or thinly traded stocks, though some newer platforms are expanding their holdings.

- Is in a high-tax state. The higher your combined federal and state rate, the more valuable the deferral becomes; a California or New York investor benefits far more than someone in a no-income-tax state.

If you checked most of these boxes, Valur can help you evaluate your options, compare exchange funds against alternatives like CRTs, and implement the right strategy, all at a fraction of the cost of traditional providers. Talk to our team.

Alternatives to Exchange Funds

Exchange funds work best for investors who can commit capital for at least seven years and have a position large enough to meet fund minimums. If those conditions don’t apply (or if you want more flexibility, liquidity, or a lower-fee structure) here are the main alternatives:

Charitable Remainder Trusts (CRTs)

A Charitable Remainder Trust lets you contribute appreciated stock to a trust, sell it tax-free inside the trust, and receive an income stream for life or a fixed term. Unlike exchange funds, CRTs provide immediate liquidity, have no lock-up requirement, and typically carry lower annual fees. The tradeoff: the trust eventually passes some assets to charity. For investors open to that charitable component – which is typically much smaller than the additional returns from tax-free compounding – CRTs are frequently a better financial outcome than exchange funds. Valur specializes in Charitable Remainder Trusts, handling everything from setup to annual administration. See our guide to CRTs or use the CRT calculator to compare your outcomes.

Opportunity Zones

Opportunity Zone investments allow you to roll realized capital gains into qualifying real estate funds in designated low-income areas and defer the tax. The structure has become less attractive as older vintages have underperformed, and the deferral window has closed for some programs. The 2025 tax bill includes new and larger benefits set to come online in 2027, and Valur is monitoring the viability of this new alternative.

Renewable Energy Tax Credits

Funding qualifying solar or renewable energy projects can generate significant federal tax credits and depreciation that can offset capital gains liability. This is a strategy to reduce taxable income rather than a deferral, and it works best when combined with other planning tools.

Charitable Lead Annuity Trusts (CLATs)

A Charitable Lead Annuity Trust reduces taxable income through charitable deductions while passing assets to heirs at the end of the trust term. It’s an estate planning tool rather than a direct capital gains strategy but can be layered with other approaches.

Here is how the main options compare at a glance:

| Exchange Fund | CRT | Opportunity Zone | Solar Credits | |

|---|---|---|---|---|

| Defers capital gains | Yes | Yes | Yes | No |

| Provides income / liquidity | No | Yes | Limited | No |

| Lock-up period | 7 years | None | 10 years | None |

| Annual fees | 0.80–1.50% | Lower | Varies, but high | None |

| Assets can pass to heirs | Yes | Partial | Yes | Yes |

| Min. size | $100k–$1M+ | None | None | $100k |

Next Steps

At Valur, we are your first stop for determining how exchange funds can help you.

We’ve built a platform that makes advanced tax planning accessible to everyone. With Valur, you can reduce your taxes by six figures or more, at less than half the cost of traditional providers.

From selecting the right strategy to handling setup, administration, and ongoing optimization, we take care of the hard work, so you don’t have to. The results speak for themselves: our customers have generated over $3 billion in additional wealth through our platform. Want to see what Valur can do for you or your clients? Explore our Learning Center, use our online calculators to estimate your potential savings or schedule a time to chat with us today!

Exchange Funds FAQs

Is an exchange fund right for me?

Exchange funds are most suitable for investors with a single stock position worth $1M or more, a very low cost basis, no need for liquidity for at least seven years, and a goal of diversifying without triggering immediate taxes. If you need income from the position, if your time horizon for liquidity is shorter than seven years, or if the position is large and fees are a real concern, alternatives like a Charitable Remainder Trust may be a better fit.

Do you pay taxes when you exit an exchange fund?

Yes, deferral does not mean elimination. When you redeem your fund shares and eventually sell the diversified basket of stocks you receive, you will owe capital gains taxes based on your original cost basis. The advantage is that you’ve had years or decades of additional compounding on the full pre-tax amount, and your gains are spread across many stocks rather than one.

Can you use an exchange fund for private company stock?

Yes, though historically it is more difficult. A growing number of funds now accept private company shares, particularly following liquidity events. Acceptance criteria and valuation requirements are more complex for private stock.

What is the seven-year rule for exchange funds?

The IRS requires investors to hold their exchange fund shares for a minimum of seven years to qualify for tax-deferred treatment. If you exit before the seven-year mark, you typically receive the lesser of your original stock value or the current fund value, lose the tax benefits, and may still owe applicable fund fees. The seven-year clock starts from the date of your contribution.

What are the downsides of exchange funds?

The main downsides are the seven-year lock-up period, ongoing annual management fees of 0.80–1.50%, limited fund availability (funds close once they reach capacity), contribution minimums of $100k–$1M+, and the fact that your original cost basis, and therefore your deferred tax liability, carries over rather than being eliminated.

What is direct indexing and how does it compare to exchange funds?

Direct indexing lets you own individual stocks in an index rather than a fund, which allows for tax-loss harvesting on individual positions. Unlike exchange funds, direct indexing doesn’t require you to contribute your concentrated position; you simply open a new account and build a portfolio. It’s generally a better fit for ongoing tax management than for a one-time concentrated position exit, and it doesn’t defer an existing embedded gain the way an exchange fund does.

Reduce your tax bill — fast

Our team of experts will help you evaluate the most promising strategies in minutes.

Talk to our expert team

Valur

Most Promising Fintech Companies 2024

On this page

- Key Takeaways

- What Are Exchange Funds?

- How Do Exchange Funds Work?

- The Tax Benefits of Exchange Funds

- Exchange Funds for Concentrated Stock Positions

- Exchange Funds: A Real-World Example

- Exchange Funds: Pros and Cons

- Is an Exchange Fund Right for You?

- Alternatives to Exchange Funds

- Next Steps

- Exchange Funds FAQs

Ready to reduce your capital gains tax?

Free 15-min consult · No obligation · Capital Gains