What is a CRUT (Charitable Remainder Unitrust)?

A CRUT, or a Charitable Remainder Unitrust, is the best way to minimize Capital Gains taxes when selling highly appreciated assets. If you have an asset(s) that have at least doubled in value and appreciated by $500k or more, you consider a Charitable Remainder Unitrust (CRUT). And despite “Charitable” being the first word in the name, CRUTs are, first and foremost, a personal wealth-creation tool.

CRUTs can increase your after-tax wealth by 50% or more in these common situations:

- You have startup equity approaching a liquidity event.

- You’re overexposed to a single stock that’s appreciated significantly. .

- You are selling private assets like real estate or another business.

I faced this exact problem in 2019, when Medallia, the startup I worked for, was preparing to IPO. After researching all my options, I thought: if billionaires like Phil Knight, the founder of Nike, use CRUTs to reduce their capital gain taxes, why can’t I?

This isn’t some loophole or gray area. CRUTs have been a stable part of American tax law since the beginnings of the country, Benjamin Franklin included charitable trusts in his will and the last major reforms were enacted in 1969. Wealthy families and their advisors have used them for hundreds of years; they just haven’t been accessible to individuals without a family office.

That’s why I founded Valur. We make it easy to understand whether a CRUT, or other tax advantaged structure makes sense for your situation, build one optimized for your specific assets and goals, and handle all the ongoing administration and optimization.

Key Takeaways

Selling inside a CRUT means no capital gains tax when selling your appreciated asset(s). 100% of your sales proceeds get to be reinvested which typically leads to 70-150% higher post tax returns.

That larger reinvested base (30-100% bigger than what you’d have after a taxable sale) compounds year after year. The return gap between a CRUT and a direct sale widens over time due to compounding; it doesn’t stay flat.

A CRUT accepts any appreciated asset with no reinvestment restrictions. A 1031 exchange, Opportunity Zone fund, or installment sale can’t match that. A CRUT also gives you an upfront charitable deduction of roughly 10% and a growing annual income stream on top.

How does a CRUT work?

A CRUT is a tax-exempt irrevocable trust similar to an IRA. You put appreciated assets into the trust, the trust sells them without paying any capital gains tax, and you receive annual distributions for the length of the trust. When the trust ends, whatever is left goes to a charity you choose.

The word “charitable” in the name is misleading. People hear it and assume CRUTs are primarily a charitable vehicle but the irony is they are primarily a personal wealth creation tool. The IRS’s conservative estimate is you get at least 90% of the trust assets.

How it works, in five steps:

- You transfer appreciated assets (stock, real estate, crypto) into the trust.

- The trust sells them. Because the trust is tax-exempt, no capital gains tax is triggered.

- The full pre-tax proceeds stay invested and continue to grow and compound.

- You receive annual distributions, a fixed percentage of the trust’s value each year (you can also defer those distributions if you want).

- When the trust ends, the remainder goes to a charity you’ve selected. You can change which charity at any time.

Most CRUTs are structured with annual distributions payouts between 5% and 11%. The trust can be set up a set number of years, your life or you and your spouses life.Most people choose a lifetime because the longer you compound pre-tax wealth, the more you get out of the deferral. A lifetime trust on a $1 million gain at age 35 will produce 5x more wealth than a 10-year trust on the same gain. (You can run the numbers for yourself here.)

What are the Types of CRUTs?

The type of CRUT you choose determines how and when you receive your distributions. Each version has its own advantages and disadvantages. The right choice for you depends distribution goals and timeline. There are three main structures:

Standard CRUT

A Standard CRUT pays you a set percentage of the trust’s value every year, regardless of what the trust actually earned. If you have a Standard CRUT with a 7% payout on a $1 million trust, you get $70,000 in year one. If the trust grows to $2 million, you get $140,000. If it drops to $800,000, you get $56,000.

This is the simplest structure. You know the payout rate upfront, and your distributions track the trust’s performance over time. It’s a good fit for people who want predictable distributions.

NIMCRUT (Net Income with Makeup Charitable Remainder Unitrust)

A NIMCRUT only distributes the lower of your fixed percentage or the trust’s actual realized income for the year. If the trust earns less than it owes you, the difference accrues in a “makeup account” (a running ledger of what the trust still owes you) and paid out in future years when the trust earns more.

Why would you want this? Because you can defer distributions, that means more tax deferred growth e.g. the higher ROI. When you’re ready, the trust starts paying out your owed percentage for that year plus the years of accumulated owed distributions.

That combination of deferral and catch-up makes NIMCRUT;s the highest-return CRUT structure. If you’re focused on maximizing total wealth, you’re setting up the trust for a long period and can afford to wait on income in the early years, a NIMCRUT is the most popular choice.

Flip CRUT

A Flip CRUT starts as a NIMCRUT and converts (“flips”) to a Standard CRUT after a specific triggering event, usually the sale of an illiquid asset or a specific calendar date.

This is the go-to structure when you want predictable distributions at some point in the future e.g. in 10 years after you retire or after you sell your dental practice. During the NIMCRUT phase, the trust isn’t forced to sell an illiquid asset to meet distribution obligations. Once the trigger event happens and the asset is sold, the trust converts to a Standard CRUT and begins consistent distributions.

It’s also useful if you want a built-in transition from a growth phase to an income phase. If you’re 10-15 years from retirement and want the trust to compound aggressively now and then switch to predictable distributions later, a Flip CRUT does that automatically.

CRUT Comparison

CRUT Case Study

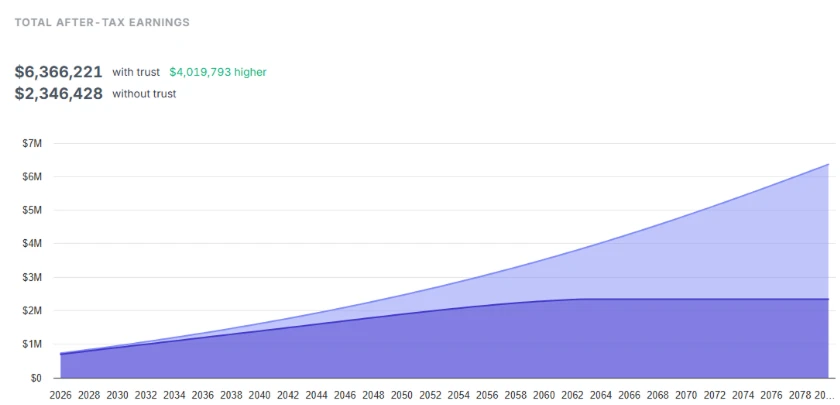

Meet Annie. She’s a married 30-year old. She joined a Bay Area startup early, exercised her stock options for $10,000 total, and can now sell her shares for $1 million after the company’s IPO. That’s a $990,000 gain.

If she sells her shares in a normal taxble account, she would owe roughly $320k in federal and state capital gains taxes (about 32% combined in California). She would then be able to reinvest the remaining $680k.

If she contributes those shares to a lifetime CRUT before selling:

- The trust sells the shares with no capital gains tax. The full $1 million stays invested.

- She gets an immediate charitable income tax deduction of roughly $100,000 (about 10% of the contributed value).

- She draws annual distributions for the rest of her life, a fixed percentage of the trust’s value.

- The trust is compounding on a base that is $320k larger from day one ($1 million v. $680k).

Over the life of the trust, Annie ends up with $4 million more after taxes than she would have kept from a direct sale. That’s in addition to the trust making a $3.6 million gift to charities of Annie’s choice at the end of the trust.

That $4 million difference comes from one thing: selling inside a tax-exempt trust means reinvesting the full pre-tax proceeds. The deferred tax dollars compound alongside your principal for the entire life of the trust.

At an 8% annual return, $1 million in deferred taxes grows to roughly $2.15 million over 10 years and $4.7 million over 20 years. All of that growth comes from keeping the government’s share invested instead of handing it over at the point of sale.

CRUT vs. No Trust: Wealth Impact Calculator

Estimate your extra payout from a $1M charitable remainder trust.

Married

Single

What are the tax benefits of a CRUT?

1. Tax deferral and compounding

This is where most of the value comes from. When you sell inside a CRUT, 100% of the proceeds remain invested. In a normal taxable sale, federal capital gains tax alone takes 20%+ of the proceeds. That difference compounds. Year after year, the CRUT’s larger base generates more returns, which in turn generate more returns. The gap between the CRUT portfolio and the after-tax portfolio gets wider every year the trust runs.

This is why lifetime trusts tend to produce the best outcomes. More time means more compounding. More compounding means greater returns.

2. Upfront charitable income tax deduction

When you fund a CRUT, you get an immediate charitable income tax deduction. For most CRUTs, that works out to a deduction worth roughly 10% of what you put in. For Annie’s $1 million contribution, that’s roughly a $100,000 deduction she can use to offset other income in the year she funds the trust. If Annie’s marginal income tax is 50%, that would mean $50,000 in income tax savings in year 1. You can apply this deduction against up to 30% of your adjusted gross income in the year you fund the trust, and carry any unused portion forward for up to five years.

3. Income smoothing

Instead of recognizing a $1 million gain in a single tax year (which would push Annie into the highest capital gains bracket and trigger the 3.8% Net Investment Income Tax), a CRUT spreads distributions over many years. Each annual distribution is taxed based on Annie’s income in that specific year.

For anyone with big, lumpy income events (an IPO, a real estate sale, a business exit), this makes a real difference. The effective tax rate on the same underlying gain can drop from 23.8% to as low as 0%, depending on how the distributions are spread and what other income you have in those years.

What is the downside of a Charitable Remainder Unitrust?

Reduced liquidity

A CRUT distributes a fixed percentage of its value annually, typically 5% to 11%. If you contribute $1 million and have a 6% payout rate, you’ll receive roughly $60,000 in year one. You cannot access the remaining $940,000 outside of that scheduled distribution.

You need to identify and plan for near-term needs, such as a tax bill, a home purchase, or your child’s college tuition. If you need access to most of your capital within the next 5 years, a CRUT probably isn’t the right move. The compounding advantage needs time to build, and the liquidity constraint means you need to be comfortable with the payout schedule before you commit. That being said you can defer your distributions in a CRUT so you can take multiple years of distributions in a year.

Irrevocability

Once assets are placed in a CRUT, the decision can’t be reversed. The trust owns the assets. You keep the right to annual distributions AND you can change the charity at any time; but you can’t reclaim the principal, change the payout rate, or dissolve the trust. This is why the right time to evaluate a CRUT is before you contribute an to the trust.

How do you set up a Charitable Remainder Unitrust?

Setting up a CRUT involves four key decisions: what assets to contribute, which type of CRUT fits your situation, what payout rate makes sense for your income needs, and who will handle the ongoing administration.

In the past, this meant finding a specialized trust attorney, negotiating fees, making all those structural decisions largely on your own, and then managing ongoing administration (annual valuations, tax filings, distribution calculations) on your own for the life of the trust. That complexity is what kept CRUTs out of reach for most people. Not the structure itself, but the friction and effort of implementing it.

Valur makes the trust decision, set up and administration seamless. Our calculators and team help you understand and quantify the benefits and tradeoffs between tax mitigation options, our platform enables you to create and access your trust documents for free in minutes and our team specializes in taking care of all of the ongoing administration and trust optimization so that you don’t have to. Our customers have generated over $3 billion in additional wealth through the platform.

One thing to be clear about: Valur doesn’t manage your money. You (and your investment team) keep full control over how the trust’s assets are invested. We handle the administration and trust optimization, you (or your financial advisor) handle the investment decisions.

Next Steps

Run the numbers. Our calculator lets you plug in your own asset, gain, age, and payout rate.

Talk to us. If the math looks interesting, schedule a call with our team. We’ll walk through your specific situation and help you figure out if a CRUT (or another structure) is the right fit.

Keep reading. We have detailed guides on every aspect of CRUTs and other tax planning strategies:

CRUT FAQs

CRUT stands for Charitable Remainder Unitrust. It’s a tax-exempt irrevocable trust created under IRC Section 664 (part of the tax code since 1969). You contribute appreciated assets, the trust sells them without triggering capital gains tax, and you receive annual distributions (a fixed percentage of the trust’s value) for a set term or your lifetime. When the trust ends, the remaining assets go to a charity you’ve chosen. The IRS grants three tax benefits in exchange: capital gains deferral, an upfront charitable income tax deduction, and income smoothing.

Yes, for most people with highly appreciated assets with gains of $500k or more who don’t need immediate access to the full principal. Selling inside a tax-exempt trust and reinvesting 100% of the proceeds creates a compounding base that is 31% to 53% larger from day one. That advantage grows every year. The real question is whether the tradeoffs (irrevocability, limited annual liquidity, charitable remainder) fit your situation.

Two main ones: liquidity and irrevocability. You can only access trust assets through the scheduled annual distribution (typically 5-10% of the trust’s value per year). And once you transfer assets into the trust, you can’t take them back, change the payout rate, or dissolve the trust. If you need full access to your capital within the next few years, or you’re uncomfortable with an irrevocable commitment, a CRUT may not fit.

The IRS uses a “worst-in, first-out” (WIFO) method. Distributions are taxed in this order: ordinary income first, then capital gains, then other income, then return of trust corpus (which is tax-free). In practice, distributions from a trust that sells appreciated assets are typically taxed as capital gains. Over time, as the trust generates investment income, the character of distributions may shift. The main advantage is that these taxes are spread over many years instead of being hit in a single year, which often results in a lower effective rate on the same total gain.

5% of the trust’s fair market value, revalued each year. The maximum is 50%. Most CRUTs are structured between 5% and 11%. Higher payout rates mean more income now and less compounding. Lower rates mean less income and more growth. The payout rate also affects your upfront charitable deduction: higher rates reduce it, lower rates increase it.

A NIMCRUT only distributes the lower of your fixed payout rate or the trust’s actual net income. Shortfalls accumulate in a makeup account, paid out in later years when earnings exceed the scheduled distribution. This lets you defer income, compound aggressively, and draw it down when you’re ready, making it the highest-return CRUT structure.

A Flip CRUT starts as a NIMCRUT and converts to a Standard CRUT when a predetermined event occurs, typically the sale of an illiquid asset or a specific calendar date. This is designed for situations where the contributed asset can’t be sold immediately (real estate, private business interests) or where you want a growth phase followed by predictable distributions (like a transition to retirement).

No. In most cases, CRUTs are irrevocable and designed to run for their full term (either a fixed period or your lifetime). Early termination is possible in very rare circumstances, typically through a court petition or by distributing all remaining assets to the charitable beneficiary. If you’re uncertain about the timeline, work through that before funding the trust.

Almost anything appreciated: publicly traded stock, private company stock (including pre-IPO equity), investment real estate, cryptocurrency, precious metals, collectibles, and business interests. The asset must be contributed before a sale is completed. A CRUT also allows additional contributions after initial funding, unlike a CRAT. That’s useful if you have multiple liquidity events over time.

Each year, the trustee determines the fair market value of the trust’s assets (typically on the first business day of the year or the trust anniversary). Your distribution equals your chosen payout percentage times that value. A 7% CRUT worth $1.2 million at valuation pays $84,000 that year. If the trust grows to $1.5 million the next year, your distribution goes up to $105,000. The percentage stays the same. The dollar amount moves with the trust’s performance.

A CRUT pays a fixed percentage of the trust’s current value each year, so distributions grow as the trust grows. A CRAT pays a fixed dollar amount set at funding, regardless of performance. For most people with appreciated assets, a CRUT wins: payouts grow with the portfolio, you can add assets over time, and IRS rules allow longer terms and higher payout rates.

Reduce your tax bill — fast

Our team of experts will help you evaluate the most promising strategies in minutes.

Talk to our expert team

Valur

Most Promising Fintech Companies 2024

Ready to reduce your capital gains tax?

Free 15-min consult · No obligation · Capital Gains