What Is The ING Trust?

The Incomplete Non Grantor trust (commonly referred to as an “ING” trust) provides a way to move taxation from the individual level to the trust level. As such, placing appreciating assets in a properly structured ING trust situated in a state with no income taxes is a way that many people can minimize state income taxes.

ING trusts do not provide income tax benefits for New York residents because in New York incomplete gifts are taxed through to the grantor.

E.g. Carly is a California resident that has an asset with a low cost basis (such as cryptocurrency bought in 2015 or stock in a business that started from scratch). The value of the asset has increased by $2,000,000 and now Carly wants to sell the asset. If Carly does not place the asset in an ING trust she will need to pay over $230,000 in California state taxes on that income. However, Carly would not need to pay those California state income taxes if she placed the asset in an ING trust in a state with no income tax before the sale.

What Does The “Incomplete” Part of “Incomplete Non Grantor Trust” Mean?

For the purposes of trusts and taxes, a gift is complete when the person giving the gift no longer controls the gift and how it is used. Further, a gift is incomplete when the person giving the gift retains some power to get the gift (or a portion of the gift) back and/or retains some control over how the gift is used.

E.g. If I give my child twenty thousand dollars as a gift with no strings attached, I no longer have that money and I have no control over how it is used, that would be a complete gift. If I give my child twenty thousand dollars but reserve the right to take the money back if my child uses it in some way that I don’t like, that is an incomplete gift.

Complete gifts are subject to federal gift taxes and incomplete gifts are not subject to federal gift taxes. (This is why incomplete gifts are a very valuable tool for someone who is doing estate planning.)

The “Incomplete” part of “Incomplete Non Grantor Trust” means that the trust is structured such that the grantor/trustmaker retains enough control/power over the assets (e.g. retaining the right to change who benefits from the trust assets) for the transfer of assets to be seen as an incomplete gift by the IRS.

What Does The “Non-Grantor” Part of “Incomplete Non Grantor Trust” Mean?

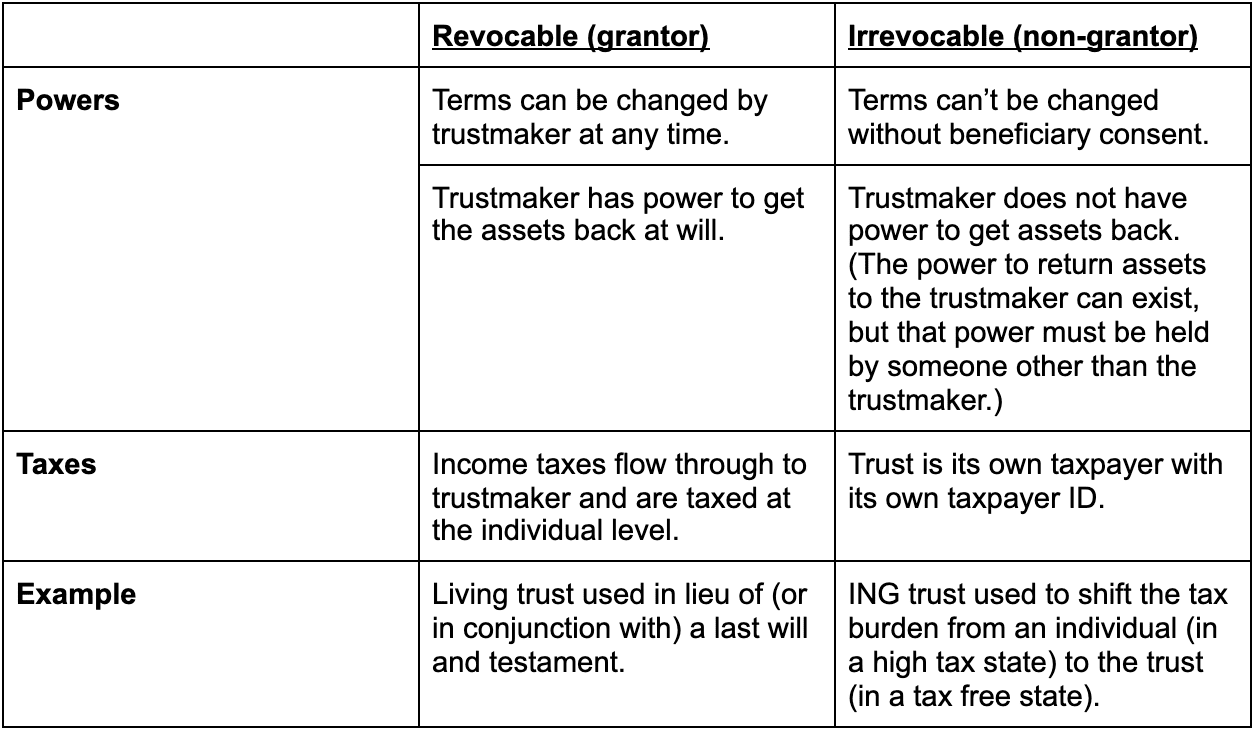

While there are MANY types of trusts, you can split all trusts into two groups: revocable (grantor) trusts and irrevocable (non-grantor) trusts. The trusts used for tax and financial planning tend to be irrevocable trusts.

In a revocable (grantor) trust the terms can be changed by the trustmaker at any time and the trustmaker can get the assets back if he/she wants. (E.g. the “living trusts” that some people use for estate planning.) An irrevocable (non-grantor) trust cannot be changed without the consent of the beneficiaries, so the trustmaker does not have the power to get the assets back.

When a trust has grantor status the income taxes flow through to the grantor/trustmaker. When a trust has non-grantor status the trust becomes its own taxpayer, so the taxation happens at the trust level and not the individual level. In other words, creating a grantor trust in a tax free state won’t help someone minimize their state income taxes, because the trust assets will still be taxed to the individual level. On the other hand, creating a non-grantor trust in a tax free state can help someone minimize their state income taxes, because the trust assets will be taxed at the trust level, and the trust exists in a state with no income tax.

Contingent vs Noncontingent Beneficiaries

The California Tax Code (specifically §17742(a)) says that a trust’s income is taxable in California “if the fiduciary or beneficiary (other than a beneficiary whose interest in such trust is contingent) is a resident” of California. In other words, in order to make the trust income not taxable in California, the beneficiary must be a contingent beneficiary.

Determining whether someone is a contingent beneficiary vs. a noncontingent beneficiary turns on a question of control. (You may be sensing a theme here: control is important when structuring trusts.)

In order to be a contingent beneficiary, one must give up control over how and when distributions are made. (See our post on Revocable vs Irrevocable Trusts for an explanation of how people give up direct control while retaining enough indirect control to feel comfortable.)

Practically, this means that instead of having defined distributions on a specific cadence, or having the right to make distributions whenever they please, a California resident will need to leave distribution decisions up to a trustee or a group of trustees who will give out distributions for the health, education, and wellness of the beneficiary(s) at their discretion.

Example: Imagine that Carl and Steve are both California residents and they both create ING trusts. Carl and Steve’s trusts are nearly identical. They have the same type of assets, they are situated in South Dakota, and they are both irrevocable with incomplete gifts. However, there is one key difference between Carl’s trust and Steve’s trust. Carl is the only beneficiary for Carl’s trust, and the trust allows him to take distributions whenever and however he wants. Steve, on the other hand, made himself a beneficiary along with his sister and his parents, and if Steve wants a distribution he needs 3/4 of the beneficiaries (himself plus two of the others) to approve. This means that Carl is a noncontingent beneficiary based on the California Tax Code, and his trust’s income is taxable in California, and Steve is a contingent beneficiary so his trust’s income is not taxable in California.

Striking a Balance

The trick with ING trusts is making sure that the grantor/trustmaker: (a) retains the specific powers the allow for the transfer of the assets into the trust to be considered an incomplete gift for gift tax purposes while also, (b) giving up the specific powers that one must forgo when creating a non-grantor trust and becoming a contingent beneficiary. This can be a difficult needle to thread, and that’s why it’s important to work with professionals.

Who Can Use An ING?

The IRS has approved the ING structure in some private letter rulings but has not issued any general formal guidance. New York passed a law that makes INGs unattractive for New York residents (New Yorkers may want to consider a New York Resident Exempt trust instead) but according to a Deloitte investigation, Californians can benefit from ING trusts so long as they are set up properly and the assets are not California sourced assets.

About Valur

We’ve built a platform that makes advanced tax planning – once reserved for ultra-high-net-worth individuals – accessible to everyone. With Valur, you can reduce your taxes by six figures or more, at less than half the cost of traditional providers.

From selecting the right strategy to handling setup, administration, and ongoing optimization, we take care of the hard work so you don’t have to. The results speak for themselves: our customers have generated over $3 billion in additional wealth through our platform.

Want to see what Valur can do for you or your clients? Explore our Learning Center, use our online calculators to estimate your potential savings or schedule a time to chat with us today!

Reduce your tax bill — fast

Our team of experts will help you evaluate the most promising strategies in minutes.

Talk to our expert team

Valur

Most Promising Fintech Companies 2024

Ready to talk through your options?

Free 15-min consult · No obligation · Estate Tax