FEATURED ARTICLE

Read More

Tax Planning for Realized Gains and Ordinary Income

Tax planning strategies for realized gains and ordinary income

GRAT Strategy Comparison: How Do The Returns Stack Up?

A GRAT is a powerful estate planning structure that allows individuals and families to reduce or eliminate estate tax as they pass on assets to the next generation. The mechanics are simple:

- An individual makes an initial contribution to a GRAT, and the trust pays back that contribution, plus interest, over the trust’s term.

- At the end of the trust’s term, the remaining assets (that is, whatever growth the trust achieved during the term, above and beyond the IRS’s statutory interest rate) are distributed to the beneficiaries free of estate tax.

- By utilizing short-term GRATs you can reduce the risk that the trust will “fail” (because you pass away during the term, negating the benefits), increase liquidity, and maximize your returns by capturing additional volatility in the investments. For more context on this short-term strategy, see here.

How do the different GRAT strategies stack up?

When it comes to choosing a GRAT strategy, there are three primary options:

- A single long-term GRAT.

- Many short-duration GRATs, each created with the proceeds from an earlier trust. (This is the “rolling GRAT” strategy we’ve covered elsewhere.)

- No GRAT planning at all; investing out of a taxable account and paying the estate tax when passing the assets on (or leveraging another method not covered here).

The best way we know how to compare these strategies is to look at the total returns — and taxes — from each over the same period of time. Let’s do that now, working with these cases and assumptions:

Cases

- Option 1 – A single 10-year GRAT.

- Option 2 – Rolling 2-year GRATs, totaling 10 years. Each GRAT after the first will be funded from the distributions from the prior GRATs.

- Option 3 – No GRATs, investing out of your own taxable account over 10 years.

Assumptions

- We’ve assumed that the market rate of return will vary by year, but we will ensure that it is consistent across the three cases for a given year so that the comparison is fair.

- IRS Discount rate / 7520 rate: 3.0% (the rate for May 2022).

- Initial funding amount: $24 million

- The grantor will gift all their remaining assets after 10 years using their remaining lifetime exemption (row “Lifetime Exemption Used”

The Results

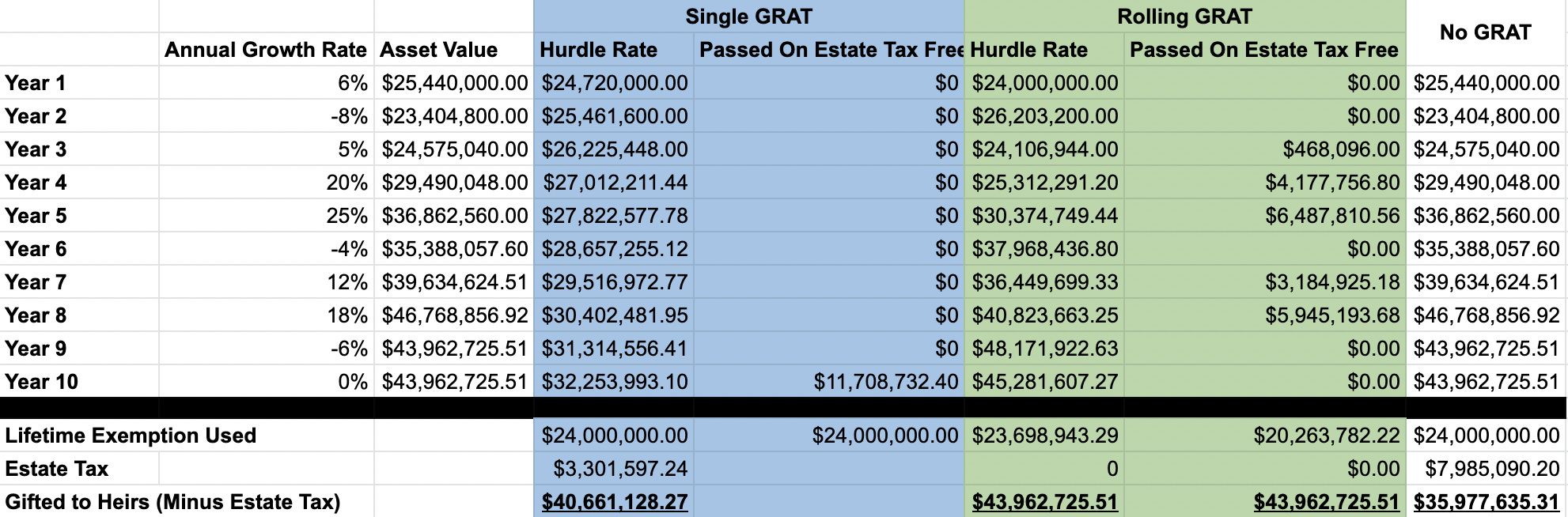

Below, we’ve outlined the expected returns, after estate taxes, from each strategy. (Though it’s worth highlighting here that the “No GRAT” scenario is the only one in which you will actually pay any estate tax.) This table outlines each individual year’s distribution to your heirs and the ultimate outcome.

It’s easy to see that the rolling GRAT approach yields the best outcome. Let’s break down what’s happening in each case:

- Option 1 – Single 10-Year GRAT: These trusts transfer money to your heirs only when the trust ends. After 10 years, this strategy would result in $40.7 million for your heirs.

- Option 2 – Rolling GRATs for 10 Years: Beginning in year 2 (the end of the first GRAT), you would start transferring the remaining assets to your heirs. Over the 10-year period, you will have transferred almost $44 million to your heirs entirely estate tax free while not using all of your lifetime exemption

- Option 3 – No GRAT: This one’s easy. By doing no tax planning, you guarantee that you will pay at least some estate tax. In this case, you’ll be leaving behind $36 million, which is about $8 million less than the optimized rolling GRAT strategy.

Next Steps

- Schedule a time to chat with our team

- Get started at no cost and with no commitment.

Related Readings

- Rolling GRATs: A Strategy To Maximize Returns

- GRAT: Grantor Retained Annuity Trust

- Guide To GRATs by Valur

About Valur

We’ve built a platform that makes advanced tax planning – once reserved for ultra-high-net-worth individuals – accessible to everyone. With Valur, you can reduce your taxes by six figures or more, at less than half the cost of traditional providers.

From selecting the right strategy to handling setup, administration, and ongoing optimization, we take care of the hard work so you don’t have to. The results speak for themselves: our customers have generated over $3 billion in additional wealth through our platform.

Want to see what Valur can do for you or your clients? Explore our Learning Center, use our online calculators to estimate your potential savings or schedule a time to chat with us today!

Reduce your tax bill — fast

Our team of experts will help you evaluate the most promising strategies in minutes.

Talk to our expert team

Valur

Most Promising Fintech Companies 2024

Ready to talk through your options?

Free 15-min consult · No obligation · Estate Tax