FEATURED ARTICLE

Read More

Tax Planning for Realized Gains and Ordinary Income

Tax planning strategies for realized gains and ordinary income

How to Avoid Capital Gains Tax With a CRUT (Charitable Remainder Unitrust)

CRUTs are the single best way to reduce Capital Gains tax on highly appreciated assets. If you have assets that have at least doubled in value and appreciated by $500k or more, you should seriously consider a Charitable Remainder Unitrust (CRUT). And despite “Charitable” being the first word in the name, CRUTs are, first and foremost, a personal wealth-creation tool.

CRUTs can increase your after-tax wealth 50% or more in these common situations:

- You have startup equity approaching a liquidity event. Your company is about to IPO or offer a tender, and you want to keep as much of your upside as possible rather than handing a third or more of it to the IRS.

- You’re overexposed to a single stock that’s grown well beyond your original investment. You know you should diversify, but selling means a massive tax hit. Maybe you’re an employee at the company, or you just made the right bet at the right time.

- You’ve built a real estate portfolio or other business you are planning to sell. You want to sell without getting crushed on the way out.

I faced this exact problem in 2019, when Medallia, the startup I worked for, was preparing to IPO. After researching all my options, I thought: if billionaires like Phil Knight use CRUTs to optimize their taxes, why can’t I?

So I set one up. Using a CRUT, I generated roughly 2.4x more wealth when I sold post-IPO, diversified into the market, and let my assets compound pre-tax. This isn’t some loophole or gray area. CRUTs have been recognized under U.S. tax law since before we declared independence, and the last major reforms were enacted in 1969. Wealthy families and their advisors have used them for decades; they just haven’t been accessible to everyone.

The problem I ran into was that the process was opaque and felt more like art than science. Finding the right attorney, understanding the tradeoffs, and handling the ongoing administration was a pain.

That’s why I founded Valur. We make it easy to understand whether a CRUT makes sense for your situation, build one optimized for your specific assets and goals, and handle all the ongoing admin that otherwise puts people off. If I’d had Valur when I set up my trust back in 2019, I could have generated an extra 50% in wealth on top of what I already saved.

Key Takeaways

Selling inside a CRUT means no capital gains tax at the point of sale. 100% of your proceeds stay invested and compounding from day one.

That larger reinvested base (25% to 53% bigger than what you’d have after a taxable sale) compounds year after year. The gap between a CRUT and a direct sale widens over time due to compounding; it doesn’t stay flat.

A CRUT accepts any appreciated asset with no reinvestment restrictions. A 1031 exchange, Opportunity Zone fund, or installment sale can’t match that. A CRUT also gives you an upfront charitable deduction of roughly 10% and a growing annual income stream on top.

You have to take the distributions over time instead of an upfront lump sum. Delaying liquidity does have the upside of lowering your effective tax rate on the same gain from 23.8% to as low as 0% through income smoothing.

What is a CRUT (Charitable Remainder Unitrust)?

A CRUT is a tax-exempt irrevocable trust. You put appreciated assets into the trust, the trust sells them without paying any capital gains tax, and you receive annual income for a set period or for the rest of your life. When the trust ends, whatever is left goes to a charity you choose.

The word “charitable” in the name is misleading. People hear it and assume CRUTs are a giving vehicle. They’re a personal wealth creation tool. The charity gets whatever is left in the trust at the end, and the IRS grants the tax benefits because of that charitable piece. But the reason you set one up is to sell appreciated assets tax-free, reinvest 100% of the proceeds, and compound on a bigger base for years or decades.

How it works, in five steps:

- You transfer appreciated assets (stock, real estate, crypto) into the trust.

- The trust sells them. Because the trust is tax-exempt, no capital gains tax is triggered.

- The full pre-tax proceeds stay invested and continue to compound.

- You receive annual distributions, a fixed percentage of the trust’s value each year (you can also defer those distributions if you want).

- When the trust ends, the remainder goes to a charity you’ve selected. You can change which charity at any time.

Most CRUTs are structured with payouts between 5% and 11%. The trust can run for a fixed period (2 to 20 years) or for your lifetime. Most people choose a lifetime because the longer you compound pre-tax wealth, the more you get out of the deferral. A lifetime trust on a $1 million gain at age 35 will produce 5x more wealth than a 10-year trust on the same gain. The math is just time and compounding.

How Much More Do You Keep With a CRUT? ($1M Example)

Meet Annie. She’s a married 30-year old. She joined a Bay Area startup early, exercised her stock options for $10,000 total, and can now sell her shares for $1 million after the company’s IPO. That’s a $990,000 gain.

If she sells directly, she owes roughly $320k in federal and state capital gains taxes (about 32% combined in California). She reinvests the remaining $680k.

If she contributes those shares to a lifetime CRUT before selling:

- The trust sells the shares with no capital gains tax. The full $1 million stays invested.

- She gets an immediate charitable income tax deduction of roughly $100,000 (about 10% of the contributed value).

- She draws annual distributions for the rest of her life, a fixed percentage of the trust’s value.

- The trust is compounding on a base that is $320k larger from day one ($1 million v. $680k).

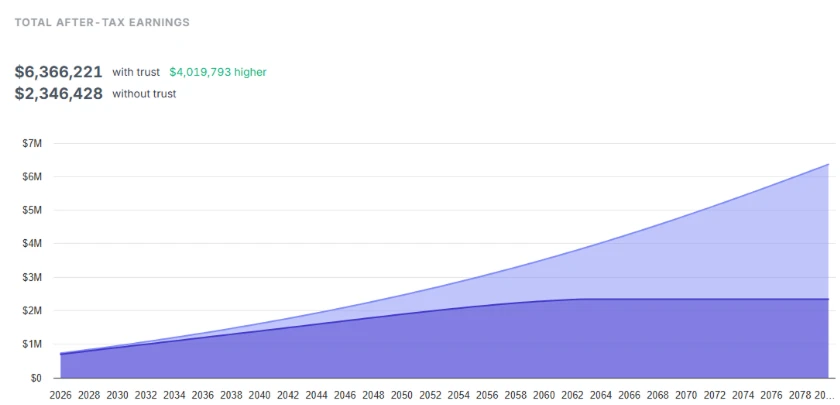

Over the life of the trust, Annie ends up with $4 million more after taxes than she would have kept from a direct sale. That’s in addition to the trust making a $3.6 million charitable contribution at the end.

That $4 million difference comes from one thing: selling inside a tax-exempt trust means reinvesting the full pre-tax proceeds. The deferred tax dollars compound alongside your principal for the entire life of the trust.

At an 8% annual return, $1 million in deferred taxes grows to roughly $2.15 million over 10 years and $4.7 million over 20 years. All of that growth comes from keeping the government’s share invested instead of handing it over at the point of sale.

CRUT vs. No Trust: Wealth Impact Calculator

Estimate your extra payout from a $1M charitable remainder trust.

Married

Single

A CRUT at a glance

The Three Tax Benefits of a CRUT

1. Tax deferral and compounding

This is where most of the value comes from. When you sell inside a CRUT, 100% of the proceeds remain invested. In a direct taxable sale, federal capital gains tax alone takes 23.8% off the top before the money has a chance to compound. On a $1 million asset, that’s $238,000 less working for you from day one.

That difference compounds. Year after year, the CRUT’s larger base generates more returns, which generate more returns. The gap between the CRUT portfolio and the after-tax portfolio gets wider every year the trust runs. In year one, the CRUT’s larger base generates roughly $70,000 more in annual returns. By year ten, that annual difference has nearly doubled.

This is why lifetime trusts tend to produce the best outcomes. More time means more compounding. More compounding means a bigger gap.

2. Upfront charitable income tax deduction

When you fund a CRUT, you get an immediate charitable income tax deduction. For most CRUTs, that works out to a deduction worth roughly 10% of what you put in. You can apply this deduction against up to 30% of your adjusted gross income in the year you fund the trust, and carry any unused portion forward for up to five years.

For Annie’s $1 million contribution, that’s roughly a $100,000 deduction she can use to offset other income in the year she funds the trust.

3. Income smoothing

Instead of recognizing a $1 million gain in a single tax year (which would push Annie into the highest capital gains bracket and trigger the 3.8% Net Investment Income Tax), a CRUT spreads distributions over many years. Each annual distribution is taxed based on Annie’s income in that specific year.

For founders and executives who have big, lumpy income events (an IPO, a real estate sale, a business exit), this makes a real difference. The effective tax rate on the same underlying gain can drop from 23.8% to as low as 0%, depending on how the distributions are spread and what other income you have in those years.

Is a Charitable Remainder Trust a Good Idea?

It depends on your asset, your gain, your timeline, and your liquidity needs. But for most people with $500k+ in unrealized gains on a highly appreciated asset, the math works out in favor of a CRUT. Here’s what that looks like across three common scenarios.

Scenario 1: Pre-IPO startup equity

You joined a company early, your shares have appreciated 3x or more, and a liquidity event is coming. The gain is large, the tax bill is painful, and you have decades ahead of you. If you contribute pre-IPO shares to a lifetime CRUT before the liquidity event, the trust sells at IPO with no capital gains tax. You reinvest the full proceeds, take annual distributions, and the compounding advantage works in your favor for the rest of your life.

| CRUT | Simple sale | |

|---|---|---|

| Initial value | $2,000,000 | $2,000,000 |

| Basis | $0 | $0 |

| Total after-tax distributions | $11,908,065 | $3,740,829 |

|

$8,167,236

218%

|

Scenario 2: Concentrated stock position

You hold a large position in a single public company (maybe you’re an employee, maybe you made an early investment), and it’s appreciated well beyond your cost basis. You know you should diversify, but selling means writing a six-figure check to the IRS. A CRUT lets you diversify without the tax hit. You contribute the concentrated position, the trust sells and reinvests across a diversified portfolio, and you receive annual distributions from the diversified base.

| CRUT | Simple sale | |

|---|---|---|

| Initial value | $1,000,000 | $1,000,000 |

| Basis | $150,000 | $150,000 |

| Total after-tax distributions | $2,593,933 | $1,345,090 |

|

$1,248,843

93%

|

Scenario 3: Appreciated real estate or a business

You’ve built a real estate portfolio or a business that has appreciated well beyond what you originally put in. You want to move into other asset classes (the stock market, bonds, alternatives), but the capital gains bill on the way out would be enormous. A CRUT works the same way here. You contribute the property or business interest to the trust, the trust sells it, and you reinvest the full proceeds without triggering capital gains.

| CRUT | Simple sale | |

|---|---|---|

| Initial value | $3,000,000 | $3,000,000 |

| Basis | $900,000 | $900,000 |

| Total after-tax distributions | $6,420,691 | $3,616,059 |

|

$2,804,632

78%

|

What Are the Disadvantages of a Charitable Remainder Unitrust?

There are real constraints you need to understand before funding a CRUT.

Liquidity

A CRUT distributes a fixed percentage of its assets annually, typically 5% to 11%. If you contribute $1 million and have a 6% payout rate, you’ll receive roughly $60,000 in year one. You cannot access the remaining $940,000 outside of that scheduled distribution.

You need to identify and plan for near-term needs, such as a tax bill, a home purchase, or your child’s college tuition. If you need access to most of your capital within the next 5 years, a CRUT probably isn’t the right move. The compounding advantage needs time to build, and the liquidity constraint means you need to be comfortable with the payout schedule before you commit.

Irrevocability

Once assets are placed in a CRUT, the decision can’t be reversed. The trust owns the assets. You keep the right to annual distributions AND you can change the charity at any time; but you can’t reclaim the principal, change the payout rate, or dissolve the trust. This is why the right time to evaluate a CRUT is before you sell an asset. Once a sale has already happened, the proceeds can’t be contributed to benefit from the tax deferral.

The charitable remainder

Whatever is left at the end of the trust goes to charity. The IRS grants tax benefits because of this charitable component. That said, most people view this as a bonus. They gain more total wealth by doing a CRUT and create a deeper legacy by donating the remainder to a cause they care about.

When doesn’t a CRUT make sense?

A CRUT is less attractive when your unrealized gain is under $500k since setup and admin costs may not be justified, when you need access to most of your capital within the next few years, when your asset hasn’t appreciated much (if your cost basis is close to the current value, there isn’t much to defer), or when you’re uncomfortable with irrevocability.

What are the types of CRUTs?

The type of CRUT you choose determines how and when you receive your distributions. Each structure has different tax, income, and compounding implications. The right choice for you depends on your asset type, timeline, and income needs. There are three main structures that create the most value.

Standard CRUT

A Standard CRUT pays you a set percentage of the trust’s value every year, regardless of what the trust actually earned. If you set a 7% payout on a $1 million trust, you get $70,000 in year one. If the trust grows to $1.5 million, you get $105,000. If it drops to $800,000, you get $56,000.

This is the simplest structure. You know the payout rate upfront, and your distributions track the trust’s performance over time. Good for people who want a more predictable income.

NIMCRUT (Net Income with Makeup Charitable Remainder Unitrust)

A NIMCRUT only distributes the lower of your fixed percentage or the trust’s actual realized income for the year. If the trust earns less than it owes you, the difference gets tracked in a “makeup account” (a running ledger of what the trust still owes you) and paid out in future years when the trust earns more.

Why would you want this? Because you can defer distributions, means more tax deferred growth e.g. the higher ROI. When you’re ready, the trust starts paying out your current percentage plus years of accumulated makeup.

That combination of deferral and catch-up makes NIMCRUTs the highest-return CRUT structure. If you’re focused on maximizing total wealth, you’re setting up the trust for a long period and can afford to wait on income in the early years, a NIMCRUT is worth considering.

Flip CRUT

A Flip CRUT starts as a NIMCRUT and converts (“flips”) to a Standard CRUT after a specific triggering event, usually the sale of an illiquid asset or a specific calendar date.

This is the go-to structure when you’re contributing something that can’t be sold right away, like real estate or a private business interest. During the NIMCRUT phase, the trust isn’t forced to sell an illiquid asset to meet distribution obligations. Once the trigger event happens and the asset is sold, the trust converts to a Standard CRUT and begins regular distributions.

It’s also useful if you want a built-in transition from a growth phase to an income phase. If you’re 10-15 years from retirement and want the trust to compound aggressively now and then switch to predictable distributions later, a Flip CRUT does that automatically.

CRUT Comparison

How Do You Set Up a Charitable Remainder Unitrust?

Setting up a CRUT involves four key decisions: what assets to contribute, which type of CRUT fits your situation, what payout rate makes sense for your income needs, and who will handle the ongoing administration.

In the past, this meant finding a specialized trust attorney, negotiating fees, making all those structural decisions largely on your own, and then managing ongoing administration (annual valuations, tax filings, distribution calculations) on your own for the life of the trust. That complexity is what kept CRUTs out of reach for most people. Not the structure itself, but the friction and effort of implementing it.

Valur makes the trust decision, set up and administration seamless. Our calculators and team help you understand and quantify the benefits and tradeoffs between tax mitigation options, our platform enables you to create and access your trust documents for free in minutes and our team specializes in taking care of all of the ongoing administration and trust optimization so that you don’t have to. Our customers have generated over $3 billion in additional wealth through the platform.

One thing to be clear about: Valur doesn’t manage your money. You (and your investment team) keep full control over how the trust’s assets are invested. We handle the administration and trust optimization, you (or your financial advisor) handle the investment decisions.

Next Steps

Run the numbers. Our calculator lets you plug in your own asset, gain, age, and payout rate.

Talk to us. If the math looks interesting, schedule a call with our team. We’ll walk through your specific situation and help you figure out if a CRUT (or another structure) is the right fit.

Keep reading. We have detailed guides on every aspect of CRUTs and other tax planning strategies:

CRUT FAQs

CRUT stands for Charitable Remainder Unitrust. It’s a tax-exempt irrevocable trust created under IRC Section 664 (part of the tax code since 1969). You contribute appreciated assets, the trust sells them without triggering capital gains tax, and you receive annual distributions (a fixed percentage of the trust’s value) for a set term or your lifetime. When the trust ends, the remaining assets go to a charity you’ve chosen. The IRS grants three tax benefits in exchange: capital gains deferral, an upfront charitable income tax deduction, and income smoothing.

Yes, for most people with highly appreciated assets with gains of $500k or more who don’t need immediate access to the full principal. Selling inside a tax-exempt trust and reinvesting 100% of the proceeds creates a compounding base that is 31% to 53% larger from day one. That advantage grows every year. The real question is whether the tradeoffs (irrevocability, limited annual liquidity, charitable remainder) fit your situation.

Two main ones: liquidity and irrevocability. You can only access trust assets through the scheduled annual distribution (typically 5-10% of the trust’s value per year). And once you transfer assets into the trust, you can’t take them back, change the payout rate, or dissolve the trust. If you need full access to your capital within the next few years, or you’re uncomfortable with an irrevocable commitment, a CRUT may not fit.

The IRS uses a “worst-in, first-out” (WIFO) method. Distributions are taxed in this order: ordinary income first, then capital gains, then other income, then return of trust corpus (which is tax-free). In practice, distributions from a trust that sells appreciated assets are typically taxed as capital gains. Over time, as the trust generates investment income, the character of distributions may shift. The main advantage is that these taxes are spread over many years instead of being hit in a single year, which often results in a lower effective rate on the same total gain.

5% of the trust’s fair market value, revalued each year. The maximum is 50%. Most CRUTs are structured between 5% and 11%. Higher payout rates mean more income now and less compounding. Lower rates mean less income and more growth. The payout rate also affects your upfront charitable deduction: higher rates reduce it, lower rates increase it.

A NIMCRUT only distributes the lower of your fixed payout rate or the trust’s actual net income. Shortfalls accumulate in a makeup account, paid out in later years when earnings exceed the scheduled distribution. This lets you defer income, compound aggressively, and draw it down when you’re ready, making it the highest-return CRUT structure.

A Flip CRUT starts as a NIMCRUT and converts to a Standard CRUT when a predetermined event occurs, typically the sale of an illiquid asset or a specific calendar date. This is designed for situations where the contributed asset can’t be sold immediately (real estate, private business interests) or where you want a growth phase followed by predictable distributions (like a transition to retirement).

No. In most cases, CRUTs are irrevocable and designed to run for their full term (either a fixed period or your lifetime). Early termination is possible in very rare circumstances, typically through a court petition or by distributing all remaining assets to the charitable beneficiary. If you’re uncertain about the timeline, work through that before funding the trust.

Almost anything appreciated: publicly traded stock, private company stock (including pre-IPO equity), investment real estate, cryptocurrency, precious metals, collectibles, and business interests. The asset must be contributed before a sale is completed. A CRUT also allows additional contributions after initial funding, unlike a CRAT. That’s useful if you have multiple liquidity events over time.

Each year, the trustee determines the fair market value of the trust’s assets (typically on the first business day of the year or the trust anniversary). Your distribution equals your chosen payout percentage times that value. A 7% CRUT worth $1.2 million at valuation pays $84,000 that year. If the trust grows to $1.5 million the next year, your distribution goes up to $105,000. The percentage stays the same. The dollar amount moves with the trust’s performance.

A CRUT pays a fixed percentage of the trust’s current value each year, so distributions grow as the trust grows. A CRAT pays a fixed dollar amount set at funding, regardless of performance. For most people with appreciated assets, a CRUT wins: payouts grow with the portfolio, you can add assets over time, and IRS rules allow longer terms and higher payout rates.

Reduce your tax bill — fast

Our team of experts will help you evaluate the most promising strategies in minutes.

Talk to our expert team

Valur

Most Promising Fintech Companies 2024

On this page

Ready to reduce your capital gains tax?

Free 15-min consult · No obligation · Capital Gains