How to File Your Trust Tax Return

Tax season is here. Today and for the next two months, our client support team has one goal: To make filing as easy on you as possible. If you are the trustee for a non-grantor trust — whether you are your own trustee or are serving on behalf of someone else — you will be responsible for filing Form 5227 (the IRS’s Split-Interest Trust Information Return). In this article, we will explain what this form is and what you need to do with it as trustee.

(Most of those reading this guide are our own clients — and we are their trust administrator. That group will receive a completed version of the form to review and sign, so this guide is more about understanding than implementation. If, instead, you are handling your own administration, please don’t hesitate to reach out to our team for help.)

How To File Form 5227

We’ll talk about the content of the form in a moment, but we want to lead with the most important thing on your plate: How to get your form filed.

Fortunately, for those working with Valur, this part is simple: Because we’ve filled the form out for you, you’ll need only to add your signature and mail the form in. Here are the steps:

1. Sign. On page 6 of the form, sign with a wet signature. (Unfortunately, this is one of many areas where the IRS hasn’t made things easy, and digital signatures are not allowed yet.)

2. Send. Mail the form to the following address:

Department of the Treasury

Internal Revenue Service Center

Ogden, UT 84201-0027

3. Retain proof of mailing! No matter how early you send your form in — and we strongly encourage you to do that well before the April 15 (or October 15 extended) deadline — mail can be slow. We have some experience with this: Several of our clients who mailed their forms in before the deadline have faced late-filing fees where the form arrived two or three weeks later. The good news is that with proof of on-time mailing, we have been able to get those late fees reversed. There are two best practices here. At an absolute minimum, you should make sure you keep your receipt showing that you paid to mail your form. Even better, consider sending by certified mail, priority mail, or even FedEx or UPS, so that you’ll have evidence of on-time mailing and proof of delivery delivery

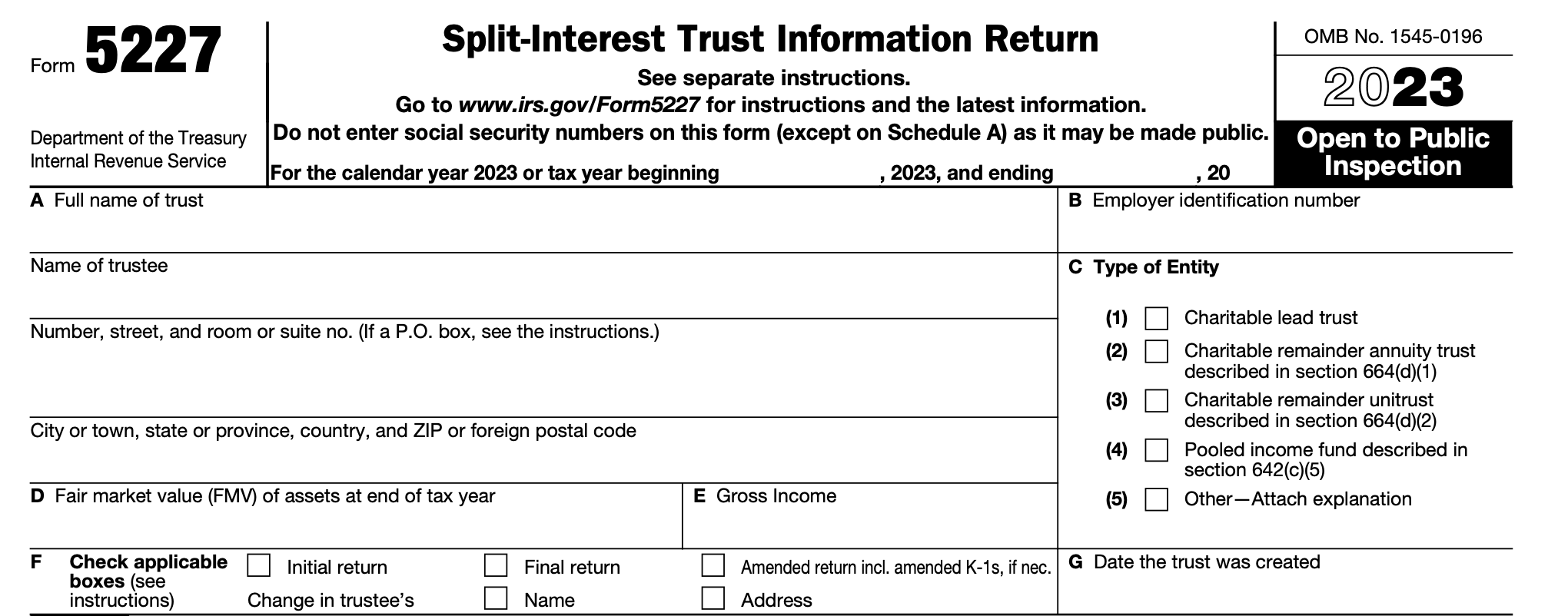

What Is Included In Form 5227?

If you work with Valur, you can simply sign and file the forms we’ve completed for you. But if you’d like to understand what you’re submitting, read on: In this section, we’ll explain the key information included in Form 5227.

Part I – Basic Identifying Information

The first thing you’ll find on the form is your trust’s basic information.

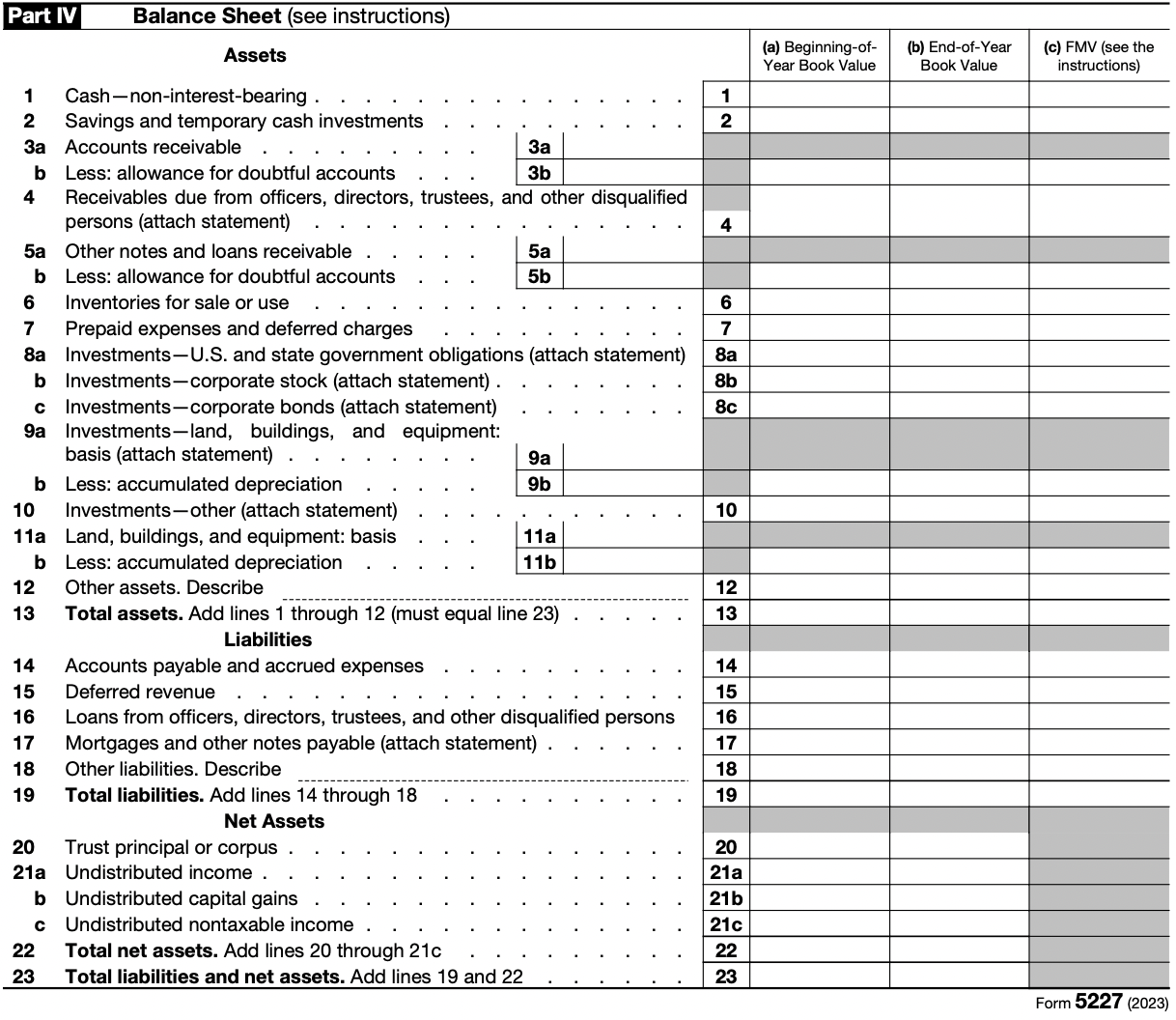

Part IV – Balance Sheet

This is an important page, as it shows the state of the trust’s assets as of the end of the year. Here you’ll see things like the trust corpus (the value you initially contributed plus any amount you have added to the trust over time), as well as the assets and liabilities that compose your trust.

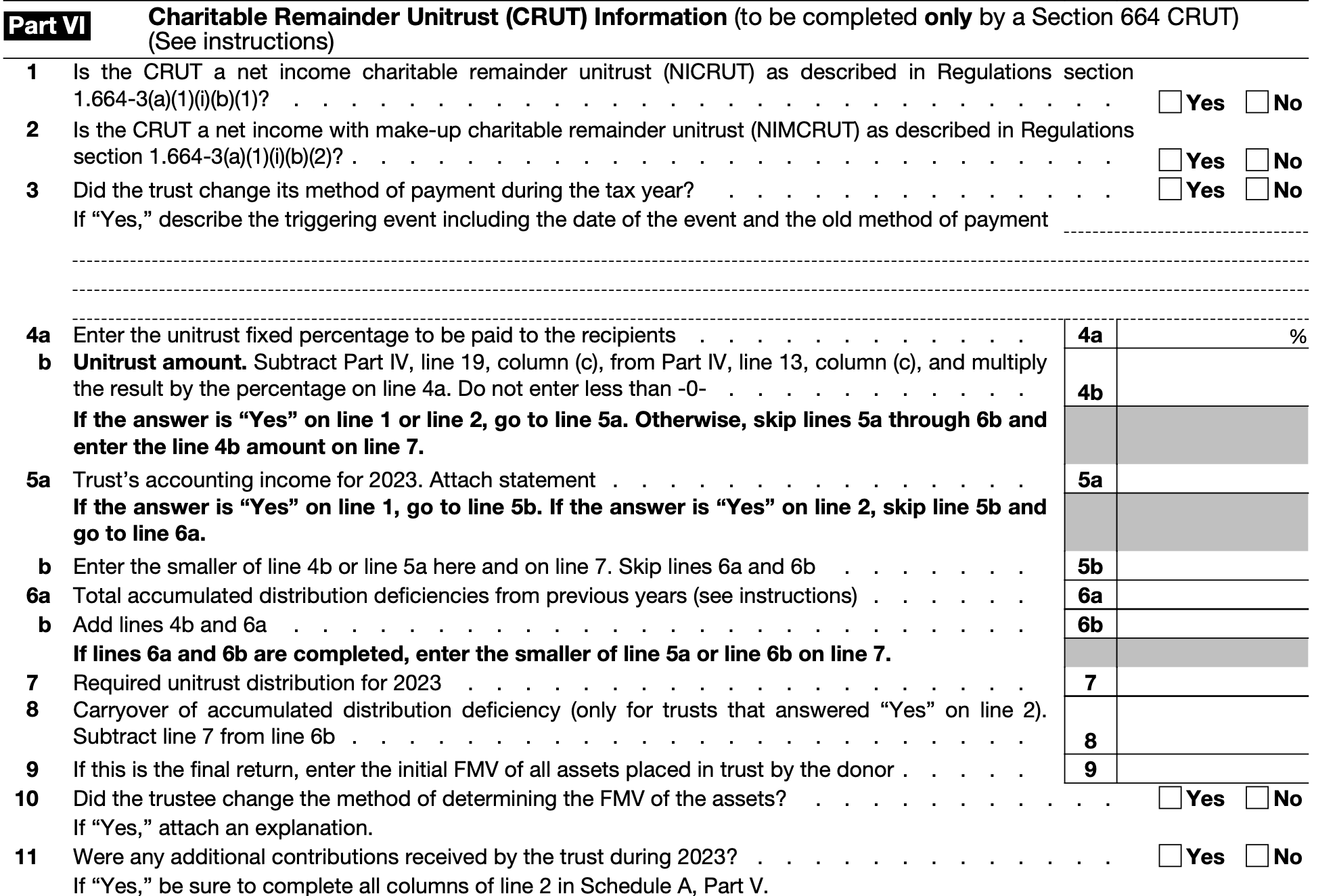

Part VI – CRUT information

This section, which applies only to CRUTs (including Standard CRUTs, NIMCRUTs, and Flip CRUTs), captures important information about how the trust is organized and how it is performing:

Conclusion and Next Steps

As we’ve explained here, if you are working with Valur, the next step is that you will shortly receive your pre-filled Form 5227 for review and filing. And as always, whether you are already working with us, whether you are looking for help with trust accounting and administration, or whether you just need a sounding board, please get in touch here or at operations@valur.io.

Reduce your tax bill — fast

Our team of experts will help you evaluate the most promising strategies in minutes.

Talk to our expert team

Valur

Most Promising Fintech Companies 2024

Ready to talk through your options?

Free 15-min consult · No obligation · Explainer