Lifetime vs Term Trust: Key Decision for Your CRT

There are key differences to understand before setting up a CRT. One of them is knowing whether you’ll choose a lifetime vs term trust. Therefore, in this article, we’ve compared these types of trusts to help you decide!

Lifetime vs Term Trust: Which is Best?

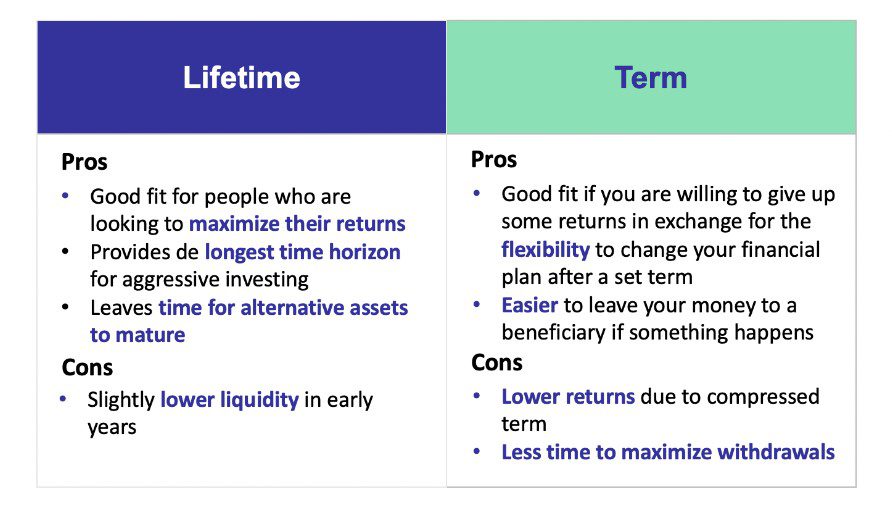

The advantages of a lifetime trust are simple: Trusts and tax planning are all about the magic of long-term tax deferral and compound growth. The longer your money grows tax free, the bigger your gains, and lifetime trusts give you more time to let that happen. Because you have your whole life to spend down the trust’s assets, moreover, you have more flexibility to invest in assets that might not ripen for a while–say, angel or other venture investments that could be illiquid for a decade. But what’s the best Charitable Remainder Trust length for you?

If you’ve read our primer on Charitable Remainder Trusts (CRTs), taken a look at our examples, or played with our various calculators, you’ll know that CRTs allow you to defer the state and federal taxes on your capital gains from the sale of startup equity, cryptocurrency, and other assets that have appreciated substantially (or are likely to do so soon). Even if you’re sold on the benefits of CRTs as a class of tax planning tools, however, you still have a key decision to make: Should you put your assets into a lifetime or term trust? (The most common length of term CRTs is 20 years, and we’ll use that number in our discussion here, but you can choose any term up to and including 20 years.)

The Benefits of Lifetime Trusts

Let’s get some hedging out of the way: This is a personal decision that depends on your family circumstances, your financial goals, and what you want your life to look like for the next 20 years or more. With that said, though, for most people, a lifetime trust will have the larger return on investment, and the reason is simple: The tax-exempt nature of CRTs allows you to defer your taxes and achieve compound growth, and the longer your money grows tax free, the bigger your gains. Lifetime trusts–by definition–will likely give you more time to let that happen.

There’s nothing fancy about the math here. If you invest $100 for 20 years at an 8% growth rate, you’ll have about $466 at the end, and about $300 after taxes; if you invest that same $100 at that same 8% growth rate but leave your money to grow for, say, 40 years–well within the reasonable life expectancy for a 35-year-old–you’ll have more than $1,300! There is, of course, some nuance here–you can always continue to invest your money outside of your trust once your term runs out, for example–but the logic holds: Deferring your taxes and letting your money grow for longer will mean greater returns, given reasonable assumptions about the performance of your investments.

Because you have your whole life to withdraw a lifetime trust’s assets, moreover, you have more flexibility to invest in assets that might not ripen for a while–say angel or other venture investments that could be illiquid for a decade. In other words, if you invest in an early-stage startup in a term CRT, by the time the investment pays out, you might only have 5 or 10 years to take advantage of tax-free compounding. If your trust runs for your lifetime, that’s less of a concern.

The Cons of Lifetime Trusts

If the case for lifetime trusts is such a slam dunk, why does anyone choose a term set up? There a few reasons. The first is psychological: For some people, it’s just easier to commit to a 20-year financial plan than to one that lasts a lifetime. There are certainly are ways to build flexibility into a lifetime trust to minimize the impact–real and psychological–of the lifetime commitment. But if this is still a concern, it’s worth emphasizing here that term CRTs also allow you to defer all of the taxes on your big exit, just like the lifetime version, and the returns can still be massive: An average of 35% greater returns with your assets in a term CRT, compared to a world in which you left your money in a taxable account.

The other major reason some people cite for choosing a term CRT is that a term trust makes it easier to leave your money to another beneficiary if something happens to you. With a term CRT, you can name a secondary (or back-up) beneficiary, so if you’re not around to collect your gains, they’ll go to someone else you designate. This could be a partner or a child (even if they’re not born yet!), or you could kick the can down the road and just say that the money should go to whoever you designate in your will. In a lifetime, trust, it’s a bit more complicated. The IRS doesn’t allow you to name a secondary beneficiary who is less than 28 years old, so kids are out, and it’s also tough to shoehorn even older people–say, your partner–in; if you’re both younger than about 41, you won’t have this option. And if you don’t have a secondary beneficiary, if the trust outlives you the full value will go straight to your chosen charity.

The Drawbacks of Lifetime Trusts

With that said, we offer a strategy that can help you work around these limitations to make sure that your money stays in your family. The strategy is called a “Wealth Replacement Trust” or “Irrevocable Life Insurance Trust,” and it’s a common tool for precisely this situation. The way it works is that you set up a lifetime trust, and then the trust buys a life insurance policy to cover the value of the trust assets–or, really, whatever value you want to pass on should the worst happen. Life insurance is so cheap for people of prime working age that you can buy a policy to cover, say, $5 million of gains for a very small fraction of the total returns from your trust. For that reason, if you don’t mind the idea of a lifetime commitment, a Wealth Replacement Trust can help you maximize the financial returns on trust planning while minimizing (or even eliminating) the downside risk.

Next Steps

Want to know more about trusts to increase your capital gains? Read our post on how long do Valur’s CRTs last to know more! Use our Charitable Remainder Trust calculator to evaluate the potential return on investment, or schedule a meeting to chat with us.

About Valur

We’ve built a platform that makes advanced tax planning – once reserved for ultra-high-net-worth individuals – accessible to everyone. With Valur, you can reduce your taxes by six figures or more, at less than half the cost of traditional providers.

From selecting the right strategy to handling setup, administration, and ongoing optimization, we take care of the hard work so you don’t have to. The results speak for themselves: our customers have generated over $3 billion in additional wealth through our platform.

Want to see what Valur can do for you or your clients? Explore our Learning Center, use our online calculators to estimate your potential savings or schedule a time to chat with us today!

Reduce your tax bill — fast

Our team of experts will help you evaluate the most promising strategies in minutes.

Talk to our expert team

Valur

Most Promising Fintech Companies 2024

Ready to reduce your capital gains tax?

Free 15-min consult · No obligation · Capital Gains