Reducing Salary Taxes with Solar Flip Partnership Purchases

Unlocking the full potential of your salary involves strategic financial decisions beyond the earnings themselves. For employees working in startups, public or private companies, high ordinary income often leads to substantial tax burdens. But there’s a powerful strategy that can increase take-home income by 50% or more: purchasing solar projects.

This article shows how purchasing solar assets can offset nearly upto 90% of your salary taxes, turning tax liability into wealth building.

But first, let’s cover the core tax benefits that make solar project purchases such a powerful tax saving tool.

What are the Financial Benefits of Buying Solar Projects?

Buying qualified solar projects can significantly reduce the taxes you pay on your salary. The core tax advantages of owning solar projects are massive, we’ve explained them in detail in this article.

In summary, the financial benefits you receive are:

- Tax credits: a dollar-for-dollar reduction in the amount of taxes you owe. The government lets you deduct a percentage of the amount you spend on a solar project from your federal taxes.

- Depreciation: the amount of value that a physical asset loses over time. From a tax standpoint, it’s important because you may be able to take a deduction for this amount, reducing your taxable income and saving money on your taxes.

- Income stream: solar projects also typically include 20-30 year income streams tied to the sale of energy produced by the project.

Salary Case Study Walk-Through

Mary is a lawyer in California and Mary is married filing jointly. In 2026, she will earn $1,000,000. As a result, she expects to have a substantial tax bill of approximately $503,000 in federal and California taxes in 2026. Assuming she falls into the highest federal marginal tax bracket of 37% and California’s highest marginal tax rate of 13.3%.

Purchasing a qualifying solar project, however, could earn Mary significant tax credits, depreciation deductions, and ongoing income to mitigate her high tax burden. Let’s walk through how she can use a solar project to reduce her taxes in 2026.

Imagine that she chooses to contribute $200,000 in a flip partnership (you can read more about that structure here) solar project this year. As a result of this purchase, she could reduce her tax bill in 2026 by $286,150 and save an additional $42,154 of taxes in the following five years. Here are the numbers:

Situation Overview:

- Income: $1,000,000 in 2026

- Expected taxes without solar benefits: $503,000

Solar Impact:

- Purchase Amount: $200,000

- Tax Savings: up to $286,150 in year 1

Total Tax Savings:

As a result, Mary’s total tax bill will drop from $503,000 to as low as $216,850. That’s a total reduction in federal and state taxes of up to $286,150 in year 1, or 143.1% of the $200,000 purchase amount From Years 2-6, there’s an additional $42,154 in state tax savings — a 21.1% return on the $200,000 purchase amount.

- Tax Credits: $158,400 in tax savings in the first year, or 79.2% of the initial purchase amount

- Federal Level Depreciation: $117,216 in tax savings, or 58.6% of the initial purchase amount. (100% of this depreciation credit is available in year 1; federal depreciation saving calculations are based on highest federal marginal tax rate of 37%.)

- State Level Depreciation: $52,688 in tax savings, or 26.3% of the initial purchase amount. (Up to 20% of this depreciation credit is available in year 1, and the remainder will be spread over the following five years; state depreciation saving calculations are based on highest state marginal tax rate of 13.3%.)

- Total Income: Mary is also expected to receive an annual income stream of 1% of the purchase amount, which would be roughly $2,000 in the first year and about $10,000 total over five years on a $200,000 purchase amount. While projections are subject to variation, these estimates are based on typical performance and current tax law.

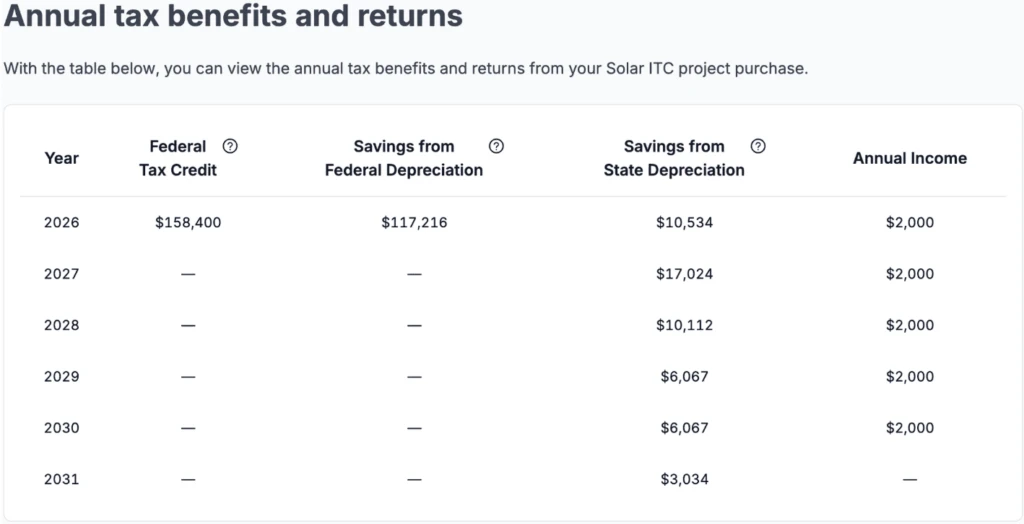

Year-by-Year Tax Savings:

Below, you can see the year-by-year tax savings from tax credits and Federal and State depreciation for Mary taking into account their particular situation.

See your potential savings with your own numbers using our online calculator here.

Tax credits and depreciation are subject to limitations based on the type and amount of income you’re applying them against in a given calendar year. However, any unused credits or depreciation can be carried forward to future years—they don’t expire or get lost. You can read more about these limitations here.

What if Mary chose not to purchase a solar project?

This is a common question: How would Mary do if she simply paid her taxes and invested the remaining money? This is a pretty simple comparison. If Mary doesn’t put $200,000 into the solar project, she would owe more than that in taxes.

Situation Overview:

- Tax bill: $503,000

- Amount not put in solar: $200,000

- Total Missed Tax Savings & Cashflow from Solar: $340,304

- Net Loss: – $140,304

Results:

If Mary simply paid her taxes, she’d owe the full $503,000. By contrast, participating in the flip partnership would generate about $340,304 in tax savings and cash flow. Subtracting the $200,000 cost of the solar purchase, that’s a net gain of $140,304 compared to doing nothing.

The key point: the $200,000 she put in solar is money she’d otherwise send to the IRS and never get back. Instead, solar allows her to redirect those “lost dollars” into something that generates additional tax savings, produces cash flow, and contributes to a cleaner environment.

Some people try to compare this to investing the same amount in the stock market—but that’s not an apples-to-apples comparison. You invest after-tax dollars in the stock market. With solar, you’re putting pre-tax dollars—money you’d otherwise send to the IRS—to work for you.

Material Participation Requirement

Since Mary is using the tax incentives to offset active income, she’s required to materially participate in the solar business for it to be considered an active business. This allows her to apply the tax benefits against her W-2 income (active income). You can learn more about material participation on our blog post or watch our explainer video.

Conclusion

Purchasing solar projects can be an effective strategy for high-income earners with significant ordinary income to reduce their tax liability.

How can you go about buying qualified projects? It’s relatively simple: Valur has partnered with reputable developers to make solar projects accessible to high-income earners. We help you identify and evaluate available opportunities, compare different project options, and visualize the potential benefits—using a calculator tailored to your specific income situation.

From there, we’ll help you seamlessly finalize your purchase—with no fees charged to you by Valur.

To learn more you can schedule a call with us here.

Need some help to understand which if this is the right fit for you?

Related Readings

About Valur

We’ve built a platform that makes advanced tax planning – once reserved for ultra-high-net-worth individuals – accessible to everyone. With Valur, you can reduce your taxes by six figures or more, at less than half the cost of traditional providers.

From selecting the right strategy to handling setup, administration, and ongoing optimization, we take care of the hard work so you don’t have to. The results speak for themselves: our customers have generated over $3 billion in additional wealth through our platform.

Want to see what Valur can do for you or your clients? Explore our Learning Center, use our online calculators to estimate your potential savings or schedule a time to chat with us today!

Reduce your tax bill — fast

Our team of experts will help you evaluate the most promising strategies in minutes.

Talk to our expert team

Valur

Most Promising Fintech Companies 2024

Ready to talk through your options?

Free 15-min consult · No obligation · Ordinary Income